The 43 Percent: How Debt Interest Eats Pakistan Before It Feeds a Child

The single biggest line in the budget, and why it strangles everything else

By Asad Baig • Written from outside Pakistan • June 2026 • Approx. 22-min read

If one number defines this budget, it is the Rs 8,054 billion the government will pay in a single year as interest on money borrowed in the past. That is about 43 percent of all federal spending. It builds nothing. It teaches no child, treats no patient, opens no road. It is simply the price of old debt, and it is by far the biggest item in the entire budget.

I want to walk you through this one number, because once you understand it, you understand why there is never enough for anything else. Where it goes, why most of it is owed to our own banks, why it falls so slowly, and what I believe it really is. For the full budget around it, read where every rupee of the budget goes. For my anger about it in full, read where is the plan.

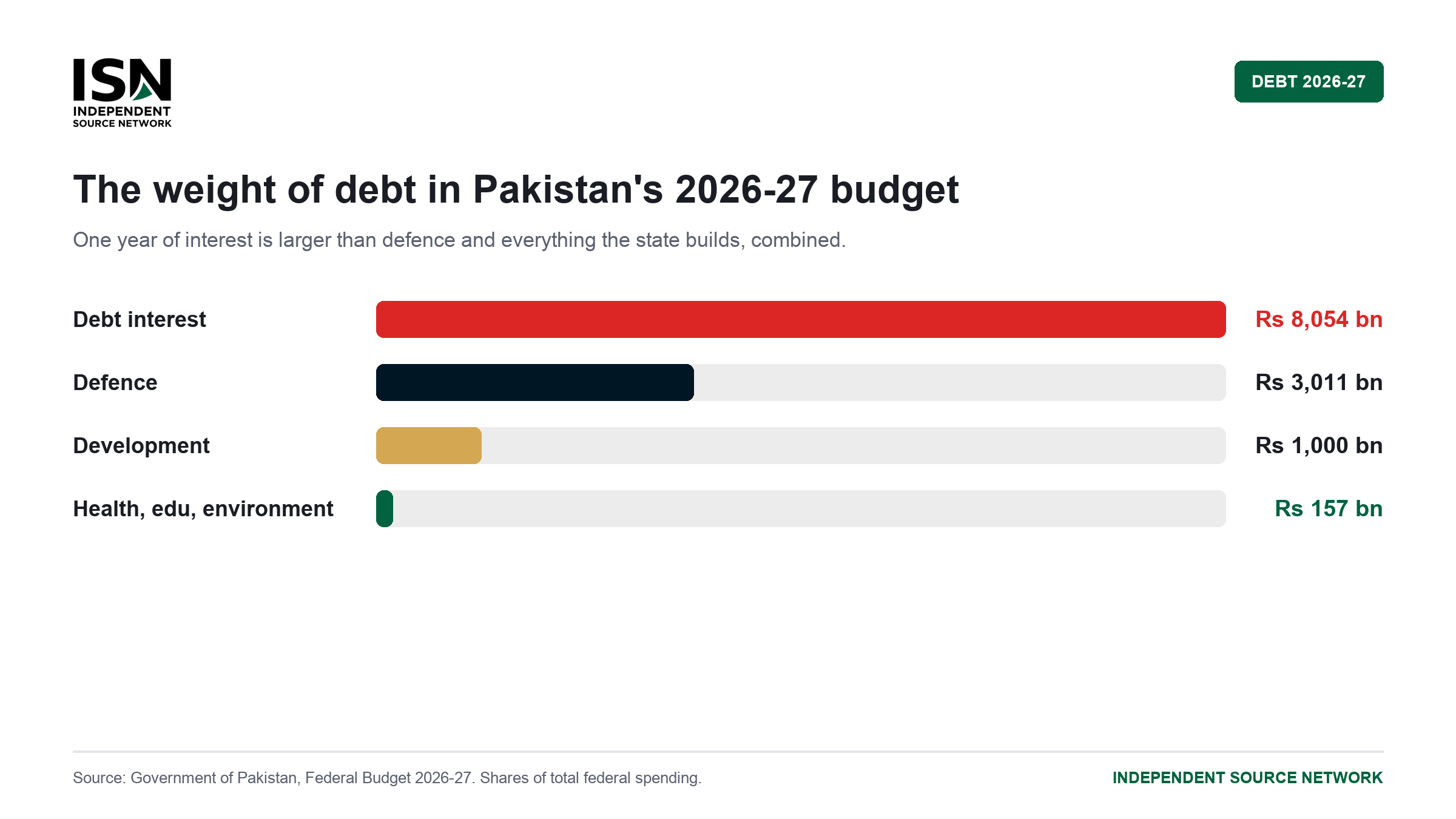

How much of Pakistan's budget goes to interest?

In 2026-27, Pakistan will spend about Rs 8,054 billion on interest, roughly 43 percent of all federal spending, the single largest line in the budget, larger than defence and the entire development programme put together. It eats close to two-thirds of all the revenue the centre keeps after paying the provinces. In plain words, before a single school, road or hospital is paid for from the government's own money, interest has already taken most of it, and the state has to borrow again to pay for everything else.

That is the weight of debt, in your hand. Now let me show you how it got so heavy.

The line that towers over everything

This number is so big that it changes how you must read every other line. Put it beside the major spending heads and you will see what I mean.

One year of interest is larger than defence and everything the state builds, combined.

| Spending head | Rs billion | Share of budget |

|---|---|---|

| Debt interest (mark-up) | 8,054 | 42.9% |

| Defence | 3,000 | 16.0% |

| Grants and transfers (incl. BISP) | 2,680 | 14.3% |

| Pensions | 1,169 | 6.2% |

| Subsidies | 1,091 | 5.8% |

| Running of civil government | 1,071 | 5.7% |

| Development programme (PSDP) | 1,000 | 5.3% |

Figures in billions of rupees, FY2026-27 Budget Estimates.

Interest alone is larger than defence, development, education and health added together. It is more than eight times what the whole state builds in a year. A budget where the cost of old borrowing is bigger than the army and everything we build, combined, is not a budget that is planning a country. It is a budget that is paying off the past, and borrowing to do even that.

Where the interest goes: to our own banks

Most of this interest is owed at home, not abroad. Of the Rs 8,054 billion, about Rs 6,983 billion is interest on domestic debt, owed to our own banks through treasury bills, bonds and Islamic instruments. Only about Rs 1,071 billion is interest on foreign loans.

| Interest type | FY 2025-26 | FY 2026-27 | Change |

|---|---|---|---|

| Interest on domestic debt | 7,197 | 6,983 | -3.0% |

| Interest on foreign debt | 1,009 | 1,071 | +6.2% |

| Total debt interest | 8,207 | 8,054 | -1.9% |

Figures in billions of rupees.

This matters, and people miss it. The problem is not mainly a shortage of dollars. The problem is that the government borrows heavily from our own banking system, at high rates. And here is the part that should make a businessman angry. Every rupee the state borrows at home is a rupee that does not reach a factory in Faisalabad or a software house in Lahore. When the banks can lend to the government at a safe, fat rate, why would they lend to your business at all, except at a worse one?

So the government is not only spending your taxes. It is also eating the credit your business needs to grow. I follow this in why most of our interest is owed at home, and the money that leaves the country in the capital that flies out of Pakistan every year.

And let me clear up one confusion before it spreads. The interest I am talking about here is the government's own national debt. It is not the same as circular debt, the unpaid bills piling up inside the power sector. That is a different wound, and I deal with it in what is circular debt in Pakistan.

The debt trap, in plain words

There is a second number that explains why this never gets better quickly. It is called the primary balance, the budget once you set interest aside. On that measure the government actually takes in more than it spends, with a primary surplus of about Rs 2,828 billion.

Read that slowly, because it is the whole trap. The deficit exists almost entirely because of interest on old debt. The government runs its day-to-day affairs in surplus, and then borrows just to pay the interest it already owes. This is what a debt trap looks like. It is why the deficit shrinks only a little, even when they hold spending down.

| Balance measure | FY 2025-26 | FY 2026-27 | Change |

|---|---|---|---|

| Federal budget deficit | 6,501 | 7,020 | +8.0% |

| Primary surplus (overall) | 3,170 | 2,828 | -10.8% |

| Overall fiscal deficit (percent of GDP) | 3.9% | 3.6% | -0.3 |

Figures in billions of rupees, except the deficit ratio.

And the primary surplus, the little cushion that pays the burden down, actually shrank this year, from Rs 3,170 billion to Rs 2,828 billion. The deficit eased a touch as a share of the economy, but that improvement leans on a hope that interest rates will fall, not on the debt itself shrinking. I lay out the mechanism step by step in the debt trap, why we borrow to pay our own interest.

Bank borrowing more than doubled

The clearest sign of the trap is this. Planned bank borrowing this year rose from Rs 1,971 billion to Rs 4,012 billion. More than double, in a single year.

It follows straight from the gap. The centre keeps about Rs 11,751 billion of its own after paying the provinces, and its day-to-day spending alone is Rs 17,495 billion. The difference is borrowed, and more of it now comes from our own banks. More borrowing at home keeps rates high, high rates raise next year's interest bill, and the bigger bill forces still more borrowing. Round and round. I trace it in bank borrowing doubled, the 103 percent jump.

Before a single school, road or hospital is paid for from the government's own money, interest has already taken most of it. Then they borrow again to pay for the rest. That is the trap, and we are deep in it.

The rollover problem: why short debt costs more

There is a detail here that makes the interest line jump fast, and it is worth a minute, because it explains why a small rise in rates becomes a big hole in the budget. Much of our domestic debt is short. Treasury bills and short instruments that must be repaid and reborrowed within months.

When you borrow short, you do not lock in a cost. You go back to the market again and again, and each time you pay whatever rate it is that day. So if rates are high, the whole pile of maturing debt rolls over at that high rate within a year or two, and the interest bill climbs almost as fast as the rate. A country that borrowed long, at fixed rates, would feel a rate rise slowly, over a decade. We borrow short. We feel it almost at once.

That is why the strongest lever on this line is not a spending cut. It is the rate, and the inflation that drives it. Lower inflation lets the rate fall, a lower rate cuts the cost of rolling over the debt, and the saving shows up in a year or two. The same thing runs in reverse when inflation rises, which is what made our recent budgets so heavy.

A worked example: how the loop tightens

Let me show you the trap as a loop, not a table. Take this budget's own figures and follow them around once.

The centre keeps about Rs 11,751 billion after paying the provinces. It owes about Rs 8,054 billion in interest. So before it funds defence, pensions, salaries, subsidies or one development project, roughly two-thirds of what it kept is already gone to interest. What is left, about Rs 3,700 billion, cannot cover day-to-day spending of Rs 17,495 billion, let alone build anything. The gap is borrowed, this year Rs 4,012 billion of it from our banks.

That new borrowing is added to the old pile. Next year, interest must be paid on a bigger pile, at whatever rate the market wants when the short debt rolls over. If the rate has not fallen, the interest line grows again, the kept revenue is eaten even earlier, and the borrowing needed to fill the gap is bigger still. This is the loop. It tightens on its own, unless one of three things happens. The rate falls. The primary surplus grows. Or the economy grows faster than the debt.

A country that borrows long feels a rate rise slowly, over a decade. A country that borrows short feels it almost at once. We borrow short.

What this interest could have built

The cost of this one line is easiest to feel when you set it beside what the same money could have built. I am not pretending we can simply switch the interest off. We cannot. It is a debt we already owe. But I want you to see the size of what it costs us every single year.

| The interest bill, 8,054 | ...set beside | The gap |

|---|---|---|

| Debt interest, 8,054 | Education, 118 | About 68 times the federal education budget |

| Debt interest, 8,054 | Health, 37 | About 218 times the federal health budget |

| Debt interest, 8,054 | Development (PSDP), 1,000 | About 8 times everything the state builds in a year |

| Debt interest, 8,054 | Health, education, environment, 157 | About 51 times all three combined |

Figures in billions of rupees, FY2026-27 Budget Estimates.

One year of interest is about fifty times what we spend, at the centre, on health, education and the environment combined. That is the price of decades of borrowing, paid now, in schools we never built and clinics we never staffed. It is the clearest answer to the question every parent asks, why is there never any money for my child's school. I take that up in education, health and the smallest shares.

How they will defend it, and why I do not accept it

Now, the economists, the suited men who carry the title, will read this differently, and I will give them their say. They split into two camps.

The first says the debt is a genuine emergency. At 43 percent of the budget, interest crowds out the very things that grow an economy, schools, roads, health, so the country cannot grow clear of it without cutting the debt itself, and every year of borrowing makes the next harder. On this view, the answer is hard discipline and a falling debt.

The second says borrowing is normal, that every modern state does it, and that what matters is not the size of the debt but what it is spent on, and whether the economy grows faster than the rate of interest. A primary surplus and falling inflation, they argue, can carry the burden without cruel cuts.

Here is the honest part. Both camps agree on the arithmetic. Interest is the biggest line. It is paid for by fresh borrowing. The debt is mostly domestic and short, so its cost jumps the moment rates rise. And the strongest lever to cut it is a lower rate, which needs lower inflation. They agree on all of that. They only differ on how loud the alarm should be. I lean to the alarm. When 43 of every 100 rupees goes to interest, that is not normal borrowing. That is a country working to pay its lenders first, and its people last.

The riba factory

And I will say the thing the economists will not. I believe this interest is riba. Our government, through its Shariah boards and its Islamic banking, has all but convinced us to accept sood dressed in a beautiful Islamic shape, and yet it pays 43 percent of its budget in interest. The whole machine, turning the labour of the poor into interest for the lenders, I call it what it is. A riba factory.

Yes, they will point to America, to how it borrows and pays interest, and tell me the problem is only where the money is spent, not the interest itself. To them I have one answer. Allah and His Messenger, peace be upon him, declared war upon those who take and give riba. So I ask, plainly, is our economy then in a battle against Allah and His Rasool? That is a heavy thing to say, and I do not say it lightly. I say it because I believe it. I set out the full argument in the riba factory, an economy at war with Allah and His Rasool, and the wider scholarly debate in interest and riba.

I know not every scholar agrees with me. Some say sovereign debt is a different matter from a moneylender squeezing a poor man, and some point to the Islamic instruments the government already uses. Let them argue it. My position is on record.

Why this reaches your own life

Do not think this is a problem for the finance ministry alone. It reaches into your house, through three doors.

The first is prices. To borrow Rs 4,012 billion from the banks, the government competes for money, which helps keep rates high, and high rates raise the cost of everything you buy on credit, from a motorcycle to a small business loan. The second is jobs. When banks lend to the state at a safe, fat rate, they lend less, and dearer, to the firms that actually hire people, so investment and hiring are squeezed. The third is the missing services. Every rupee on interest is a rupee that cannot go to a school, a clinic, a road.

None of this is abstract. The interest line is why your loan costs more, why fewer jobs are created, and why your child's school has no money, all in the same year. The column of huge numbers is, in the end, a description of those three pressures on your own life.

Think of the young man who wants to open a small workshop. He goes to the bank for a loan. The rate he is offered is high, so high it would eat his profit before he hires his first worker. He does not know it, but he is standing in a queue behind his own government, which borrowed first, and bigger, at a safer rate. He walks out without the loan. The workshop is never built. The two workers he would have hired stay jobless. None of them will ever read the word "interest" in the budget, but the budget reached into their lives anyway, and closed a door.

That is what 43 percent looks like from the ground. Not a number. A door that does not open.

What could change, if they meant it

I will not only complain. Let me tell you what could actually move this line, so you can judge them against it.

The first is lower inflation and a lower policy rate. Since most of the debt is domestic and short, its cost tracks the rate closely, so steady, lasting disinflation is the strongest lever. The trouble is it needs a stability we keep throwing away.

The second is borrowing for longer. When you borrow for a few months at a time, you must refinance forever at whatever rate prevails. Borrowing through longer bonds locks the cost in and cuts the risk, though lenders charge a little more for it.

The third is a bigger, steadier primary surplus, built through a wider tax net rather than through cuts to development. I deal with the tax side in how Pakistan raises its money.

The fourth is protecting the things that grow the economy even in a hard year. If you cut development and schools to pay the debt, you weaken the very economy that is supposed to grow clear of the debt. The composition of any cut matters as much as its size.

None of these is quick. And none of them lets you simply cut the interest, the way you cut a subsidy, because it is a debt already owed. It can only be eased over years. Which is exactly why I do not accept any government telling you it is fixing this in one budget. It cannot. The most it can do is stop making it worse.

And here is the thing I want you to carry away. Every one of these levers is slow, and every one of them is boring, and none of them wins an election. A handout wins an election. A new motorway, cut with a golden scissor on television, wins an election. Quietly borrowing for longer, holding inflation down for years, widening the tax net so the rich finally pay, none of that gets a man re-elected. So it does not get done. The debt grows in the dark, between the photo opportunities, and it is your children who will pay the interest on it long after the men who borrowed are gone.

What the figures show

The weight of debt is the first fact of this budget, and every other choice bends around it.

Of every hundred rupees the government spends, about 43 go to interest. That one line is bigger than defence and development combined, and it eats most of the revenue the centre keeps after paying the provinces. The government runs a surplus on its day-to-day account and then borrows to pay the interest on debt it already carries, which is why the deficit shrinks so slowly, and why bank borrowing more than doubled this year.

The debt is mostly owed at home, so the real problem is the high rate at which the government borrows from our own banks, and the strongest cure is lower inflation, held for years. Whatever you conclude, you cannot understand this budget without putting this number first. I put it first because it is the reason there is never enough for you.

Frequently asked questions

How much interest does Pakistan pay in 2026-27? About Rs 8,054 billion, roughly 43 percent of all federal spending. About Rs 6,983 billion of it is interest on domestic debt and about Rs 1,071 billion on foreign debt.

Is interest really the largest item in the budget? Yes. At Rs 8,054 billion, it is the single largest line, bigger than defence (Rs 3,000 billion) and the development programme (Rs 1,000 billion) put together, and about eight times the development budget.

What is a primary surplus, and why does Pakistan have one? A primary surplus means the government takes in more than it spends before counting interest. Ours is about Rs 2,828 billion. It exists because the deficit is driven almost entirely by interest on old debt, not by day-to-day overspending.

Why is most of Pakistan's debt domestic? Because most of the interest, about Rs 6,983 billion, is owed at home to our own banks through bills, bonds and Islamic instruments. The core problem is the high rate at which the government borrows from its own banking system, not mainly a shortage of foreign currency.

Why did bank borrowing double in the budget? Because the centre spends far more than it keeps after paying the provinces, and fills the gap by borrowing, more of it from domestic banks. It rose from Rs 1,971 billion to Rs 4,012 billion, which tends to keep interest rates high.

What is the difference between national debt and circular debt? National debt is money the government itself borrowed, and its interest is the Rs 8,054 billion here. Circular debt is the separate pile of unpaid bills inside the power sector. Two different problems, explained in what is circular debt in Pakistan.

Can the government just cut the interest to free up money? No. Interest is a legal obligation on debt already owed, so it cannot be cut like a subsidy. It can only be eased over years through lower rates, longer maturities and a debt that grows more slowly than the economy.

Is the interest Pakistan pays riba? I believe it is, and I say so plainly in the riba factory. Not every scholar agrees, and the debate is set out in interest and riba. It is a religious and moral question, and my position on it is my own.

Does a primary surplus mean the budget is improving? It is a sign of discipline on day-to-day spending, but it does not by itself mean the debt is falling. Our primary surplus actually shrank this year, from Rs 3,170 billion to Rs 2,828 billion, so the cushion to pay down the burden got smaller even as the headline deficit eased.

How does debt interest affect ordinary Pakistanis? Through three doors. Heavy government borrowing keeps rates high, which raises the cost of your loans. It crowds out credit that would fund firms and jobs. And every rupee on interest is one that cannot fund a school, clinic or road.

Sources and notes

- Government of Pakistan, Federal Budget 2026-27: Budget in Brief, Annual Budget Statement, and Demands for Grants. All figures are Budget Estimates in billions of rupees, rounded for readability.

- Debt interest, domestic and foreign split, primary balance, deficit and bank borrowing: Federal Budget 2026-27 major spending heads and financing.

- The two readings of the debt reflect mainstream debate among economists studying Pakistan, including IMF and World Bank analyses.

- The view that this interest is riba is my own religious and moral position. I have presented the contrary view alongside it. The numbers are the government's; the judgments are mine, and I have said where.

Related reading

- The full budget: where every rupee of the budget goes

- The opinion: where is the plan

- Cluster explainers: domestic vs foreign debt, the debt trap and the primary surplus, bank borrowing doubled, the riba factory, interest and riba

- Related: how Pakistan raises its money and the capital that flies out of Pakistan every year