Domestic vs Foreign Debt: Why Most of Pakistan's Interest Is Owed at Home

Of Pakistan's Rs 8,054 billion interest bill, the larger part is owed to its own banks

By the ISN Media desk • June 2026 • Approx. 8-min read

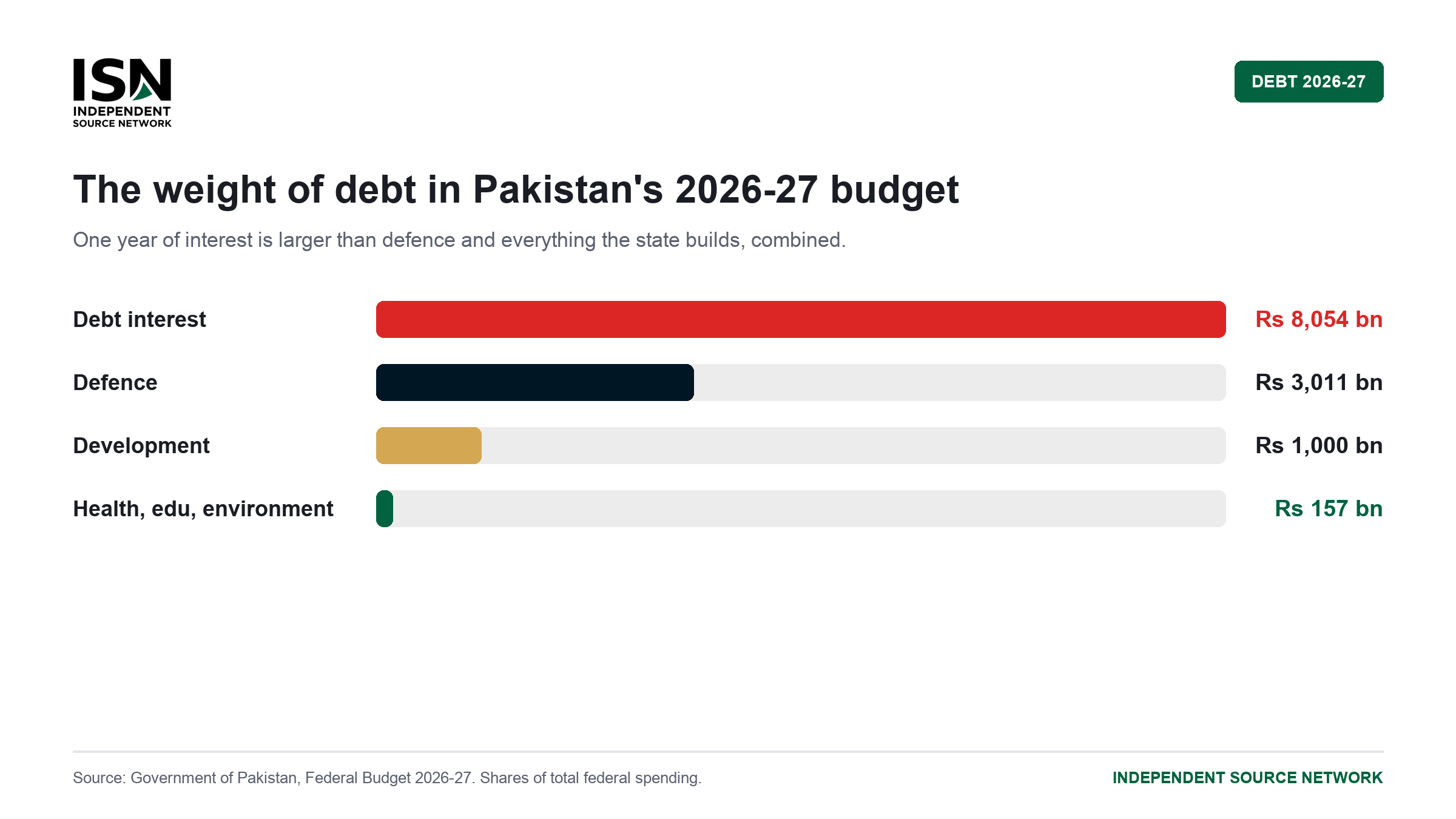

Pakistan's interest bill is the largest single item in its 2026-27 budget, and where that interest is owed shapes what the problem actually is. This explainer separates the domestic from the foreign portion, explains why the distinction matters, and sets out the effect economists call crowding out. The figures are Budget Estimates from the Government of Pakistan, in billions of rupees. It sits under the pillar the 43 percent, how debt interest consumes Pakistan's budget.

Is Pakistan's debt mostly domestic or foreign?

Most of Pakistan's interest is owed at home, not abroad. Of the roughly Rs 8,054 billion in interest the federation will pay in 2026-27, about Rs 6,983 billion is interest on domestic debt, owed to banks through treasury bills, bonds and Islamic instruments, while only about Rs 1,071 billion is interest on foreign loans. This means the core difficulty is the high rate at which the government borrows from its own banking system, rather than mainly a shortage of foreign currency.

That distinction changes how the problem should be understood.

The split, in figures

| Interest type | FY 2025-26 | FY 2026-27 | Change |

|---|---|---|---|

| Interest on domestic debt | 7,197 | 6,983 | -3.0% |

| Interest on foreign debt | 1,009 | 1,071 | +6.2% |

| Total debt interest | 8,207 | 8,054 | -1.9% |

Figures in billions of rupees.

The total interest bill, beside the major spending heads.

Domestic interest is roughly six and a half times the foreign interest. The foreign portion rose about 6 percent this year, while the domestic portion fell slightly, but the balance remains heavily weighted toward debt owed inside the country.

How domestic debt is raised

The government borrows at home mainly through three instruments. Treasury bills are short-term borrowing, repaid within months. Pakistan Investment Bonds are longer-dated. Islamic instruments, known as sukuk, raise part of the domestic debt in a Shariah-compliant structure. The buyers are largely commercial banks, which hold government paper as a safe, interest-bearing asset.

Because a large share of the domestic debt is short in tenure, it must be repaid and reborrowed frequently. This is the rollover feature: when the government borrows short, it returns to the market again and again to refinance, paying whatever rate prevails on each occasion. A rise in interest rates therefore feeds into the budget quickly, which is why the interest line is so sensitive to monetary conditions.

Why a domestic debt is different from a foreign one

A debt owed at home and a debt owed abroad pose different risks. Foreign debt must be serviced in foreign currency, so it depends on the country's reserves and exchange rate, and a currency depreciation makes it more expensive. Domestic debt is owed in rupees to domestic institutions, so it does not carry the same currency risk.

But a heavy domestic debt carries its own cost, which is the central point for Pakistan. When the government borrows large sums from the domestic banking system, it competes with private borrowers for the same pool of credit. This is examined alongside the foreign-currency dimension in our colleagues' work on the capital that flies out of Pakistan every year.

Crowding out: the cost to the private economy

The most important consequence of heavy domestic borrowing is what economists call crowding out. When banks can lend to the government at a high, risk-free rate, they have less reason to lend to a manufacturer or a small business, and every reason to charge those borrowers more. Private investment, the activity that creates jobs, ends up competing for credit against the state itself, and usually loses.

A budget that borrows about Rs 4,012 billion from the banking system in a single year is therefore not only a fiscal document. It is also a claim on the credit that the productive economy needs to grow. The scale of that borrowing is examined in bank borrowing doubled, the 103 percent jump.

Why the mix matters for monetary policy

The heavy weight of domestic debt also complicates the job of the State Bank of Pakistan. When the government is the largest borrower in the banking system, decisions about the policy rate have a direct and immediate effect on the public finances: raising rates to control inflation also raises the cost of rolling over the government's short-term debt, enlarging the interest bill. This creates a tension between the goal of price stability and the goal of fiscal sustainability that does not arise as sharply in countries with smaller or longer-dated domestic debt.

It also means that a large part of the banking sector's assets are government securities rather than loans to businesses and households. A banking system that finds it more profitable and safer to lend to the state than to the private economy is performing a narrower role than a banking system in a growing economy would, and this is one of the structural concerns economists raise about Pakistan's reliance on domestic borrowing. The wider effect on private credit is the crowding-out problem described above.

How the burden compares over time

The balance between domestic and foreign interest is not new, but the dominance of the domestic portion has grown as successive deficits were financed at home. Because each year's borrowing adds to the stock on which next year's interest is paid, the domestic interest bill tends to ratchet upward over time unless the policy rate falls or the primary surplus grows enough to slow the accumulation. This year's small dip in domestic interest, set against a rise in the foreign portion, reflects assumptions about easing rates rather than a fall in the underlying debt.

What would reduce the domestic interest bill

Because the domestic interest bill tracks the rate at which the government borrows, the most powerful lever for reducing it is a lower policy rate, which in turn depends on sustained lower inflation. Lengthening the maturity of the debt, by shifting from short treasury bills toward longer bonds, would also reduce the rollover risk that makes the bill move so quickly, though investors demand a premium to lend for longer. Both are slow processes, and neither allows the interest line to be cut in a single budget, because it is a legal obligation on debt already owed.

Frequently asked questions

Is Pakistan's debt mostly domestic or foreign? Mostly domestic. About Rs 6,983 billion of the 2026-27 interest bill is on domestic debt and about Rs 1,071 billion on foreign debt, so the larger problem is the rate at which the government borrows from its own banks.

Why does the domestic share matter? Because it means the core difficulty is not mainly a shortage of dollars but the cost of borrowing at home, and because heavy domestic borrowing crowds out credit for private business.

What is crowding out? When the government borrows heavily from banks at a high, safe rate, banks lend less, and at worse terms, to private firms. Private investment competes for credit against the state and tends to lose, which slows job creation.

How is Pakistan's domestic debt raised? Mainly through treasury bills (short-term), Pakistan Investment Bonds (longer-term) and Islamic instruments called sukuk, bought largely by commercial banks.

Does foreign debt not matter then? It matters, but differently. Foreign debt must be serviced in foreign currency and is sensitive to the exchange rate and reserves. It is the smaller part of the interest bill, though it rose about 6 percent this year.

Can the domestic interest bill be cut quickly? No. It can only be eased over time through a lower policy rate, sustained lower inflation, and longer debt maturities. It cannot be cut in a single budget because it is an obligation on debt already borrowed.

Why does so much of the banking system's money go to the government? Because government paper offers banks a safe, attractive, interest-bearing return. When lending to the state is more profitable and less risky than lending to businesses, banks hold more government securities, which is the mechanism behind crowding out.

How does foreign debt differ in its risks? Foreign debt must be serviced in foreign currency, so it is sensitive to the exchange rate and to the level of reserves; a depreciation makes it more expensive. Domestic debt, owed in rupees, avoids that currency risk but competes for domestic credit.

Sources and notes

- Government of Pakistan, Federal Budget 2026-27: domestic and foreign interest figures are Budget Estimates in billions of rupees, rounded for readability.

- The descriptions of treasury bills, bonds, sukuk and crowding out reflect standard public-finance definitions.