Projected indicators in 2031 if the Productive Capital Account framework is adopted

By Asad Baig · Lahore · May 2026 · Approx. 9-min read

What this cluster post is part of

This is one of four cluster posts under the Productive Capital Account: a reform proposal for Pakistan's FCY system. The companion posts are PCA eligibility, caps, and mechanics explained, the five FATF-compliant safeguards of the Productive Capital Account, and why FCY reform has not happened in 33 years.

This post focuses on the projected outcomes if Pakistan adopts the PCA framework. Five-year outlook. Indicator-by-indicator projection. Methodology and caveats. Read it as a scenario analysis. The figures are projections based on comparable country experience and Pakistan-specific conditions, not predictions. Actual outcomes depend on implementation quality and external conditions.

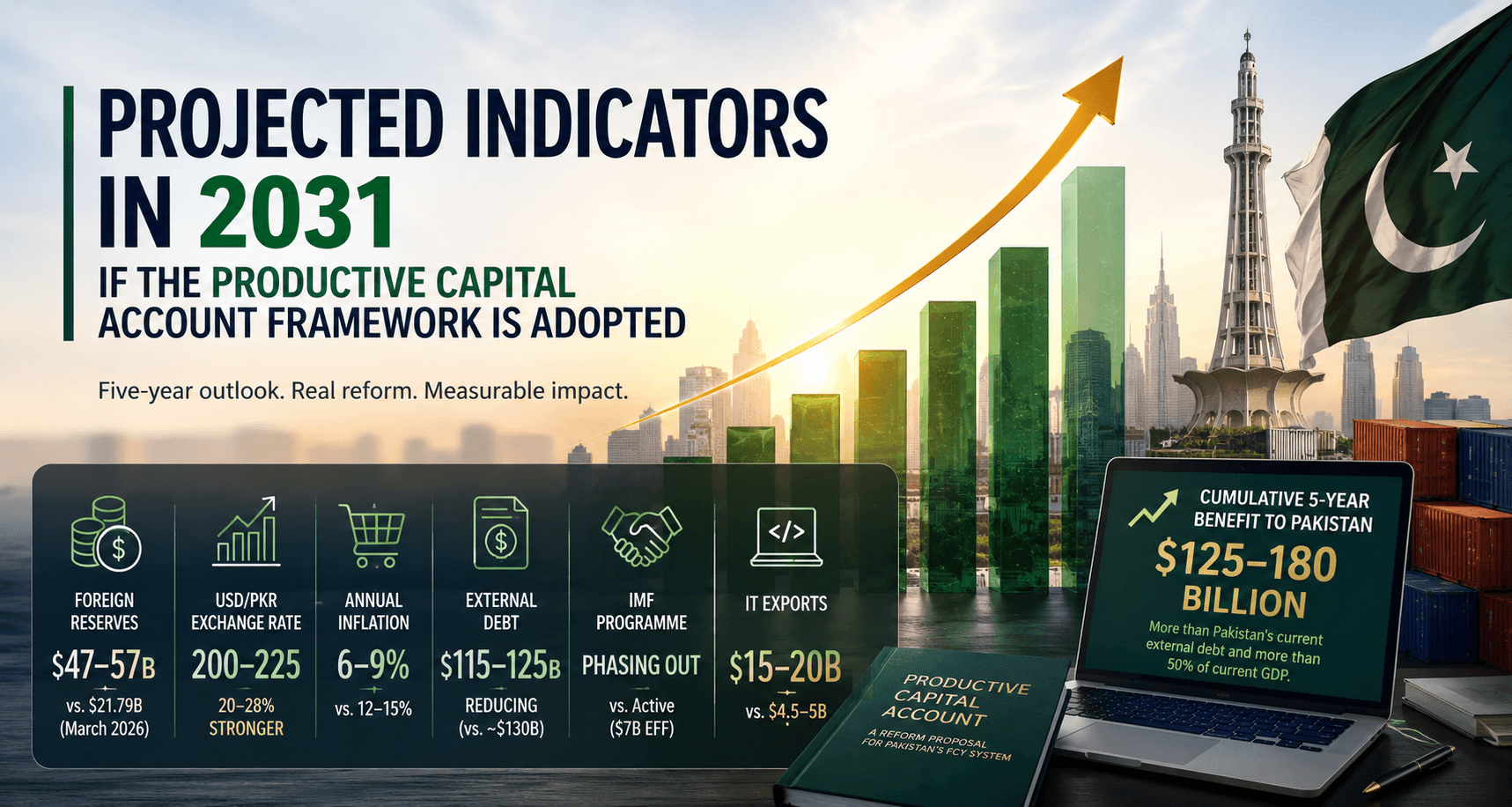

The 5-year outlook in one paragraph

Under the PCA framework adopted in 2026 to 2027 with phased rollout completed by 2028, Pakistan's projected indicators for 2031 are: foreign reserves of $47 to 57 billion (versus $21.79 billion verified in March 2026); USD/PKR exchange rate of 200 to 225 (20 to 28 percent stronger than current ~280); annual inflation of 6 to 9 percent (versus current 12 to 15 percent); external debt reducing toward $115 to 125 billion (versus current ~$130 billion); IMF programme dependence phasing out (versus current $7 billion EFF active); and IT exports reaching $15 to 20 billion (versus current $4.5 to 5 billion). The cumulative 5-year benefit to Pakistan is projected at $125 to 180 billion, more than Pakistan's current external debt and more than 50 percent of current GDP.

The projected 2031 indicators

Projected 2031 Indicators Under Pca Reform

Indicator | Current (2026) | Year 5 with reform |

|---|---|---|

Foreign reserves | $21.79B verified | $47-57B projected |

USD/PKR exchange rate | ~280 | 200-225 (20-28% stronger) |

Annual inflation | 12-15% | 6-9% |

External debt | ~$130B | $115-125B reducing |

IMF programme | Active ($7B EFF) | Phasing out |

IT exports | $4.5-5B | $15-20B |

Each projection rests on specific mechanism assumptions that are themselves grounded in comparable country experience.

How the reserves number is built

Reserves Projection, Components

Component | Projected |

|---|---|

Existing 2026 baseline | $21.79B |

Productive class repatriation (5 years) | +$25-35B |

Reduced offshore migration of ongoing flows | +$5-10B |

RDA growth + diaspora savings expansion | +$5-10B |

Reduced bilateral support need (offset) | Net positive |

Reduced IMF dependence | Net positive |

PROJECTED 2031 RESERVES | $47-57B |

The largest component is productive class repatriation. The mechanism: Pakistani productive earners (IT companies, freelancers, exporters) currently route 30 to 60 percent of foreign earnings through offshore structures (Wyoming LLCs, Mercury, Wise, UAE free zone companies, Singapore subsidiaries). Under the PCA, the operational reasons for offshore routing are eliminated, and the framework becomes operationally competitive with offshore alternatives. Conservative estimate: $25 to 35 billion in cumulative 5-year repatriation.

The second component is reduced offshore migration of ongoing earnings. Pakistani productive class earnings continue to grow. Under the current framework, growing earnings increasingly flow offshore. Under the PCA, growing earnings flow into Pakistani banks. The 5-year cumulative effect of preventing this offshore migration is $5 to 10 billion.

The third component is RDA growth and diaspora expansion. The existing RDA is growing at $2 billion per year. Under the PCA-extended framework that adds currencies (SAR, CAD, AUD) and expands eligibility to Pakistani-origin foreign citizens, the diaspora flow could grow further. Cumulative 5-year addition: $5 to 10 billion.

Why the rupee strengthens

The mechanism is straightforward dollar supply economics. More dollars entering through formal channels = stronger rupee. Less offshore migration of earnings = more formal-channel dollar supply.

The exchange rate projection of 200 to 225 PKR/USD is conservative. Some analysts working on similar models project that rates could appreciate further if the offshore wealth repatriation is more aggressive than the conservative scenario assumes. The 200 to 225 range reflects the conservative scenario.

How inflation reduces

Inflation Reduction Mechanism

Imported inflation reduces | Stronger rupee → cheaper imports → lower CPI |

|---|---|

Reduced subsidy needs | Less external support needed → less PKR creation |

Reduced borrowing | Lower borrowing → less monetary accommodation |

Combined effect | 12-15% inflation → 6-9% inflation |

Pakistan's chronic inflation is partly imported (oil, food, machinery) and partly produced by the monetary accommodation required to support the current external borrowing model. Stronger rupee reduces imported inflation. Reduced external borrowing need (because reserves are stronger) reduces monetary accommodation. Combined effect: inflation projection of 6 to 9 percent versus current 12 to 15 percent.

This inflation reduction is the single largest benefit to the working class under the PCA reform. The estimated $20 to 25 billion in 5-year household inflation savings flows directly to the 150 million working-class Pakistanis who are otherwise the primary losers under the current framework.

How external debt reduces

External Debt Reduction

Current external debt | ~$130B |

|---|---|

PCA-driven repatriation | Reduces borrowing need |

IMF programme phase-out | Reduces new borrowing |

Stronger rupee | Reduces debt service in real terms |

Projected 2031 external debt | $115-125B (reducing) |

The debt reduction is moderate over five years because servicing existing debt while reducing new borrowing takes time. The trajectory turns from accumulating debt to reducing debt, which is the more important indicator. Pakistan moves from "external debt grows faster than GDP" to "external debt grows slower than GDP and starts to decline in absolute terms".

How IT exports grow

It Exports Growth Mechanism

Currently captured in Pakistani statistics | $4.5-5B |

|---|---|

Currently held offshore (Wyoming, UAE, Estonia) | $0.5-3B |

Total actual current Pakistani IT earnings | $5-8B |

Under PCA: 90%+ in formal Pakistani statistics | $5-8B captured |

Under PCA: industry growth unleashed (5-year) | $15-20B by 2031 |

The IT exports projection has two components. First, the existing offshore-held earnings flow into formal Pakistani statistics under the PCA. This alone moves the headline figure from $4.5-5 billion to $5-8 billion almost immediately, with the difference being entirely a measurement effect rather than actual growth.

Second, the industry's growth itself accelerates under the PCA. Pakistani IT companies that no longer have to maintain Wyoming LLCs and offshore structures can deploy that energy and capital toward growth. Pakistan's 0.5 percent share of US IT outsourcing is far below capacity. Under operational conditions comparable to peer countries, the share can grow toward 1.5 to 2 percent over 5 years, producing $15 to 20 billion in IT exports by 2031.

The cumulative 5-year benefit breakdown

5-year Projected Benefit TO Pakistan ($ Billions)

Low | High |

|---|---|

$25 | $35 |

$25 | $25 |

$15 | $20 |

$10 | $15 |

$20 | $25 |

$30 | $60 |

$125 | $180 |

The components and their methodologies:

Additional reserves ($25-35B): Productive class repatriation as detailed above.

Reduced debt-service costs (~$25B): Stronger rupee reduces real value of foreign debt obligations in PKR terms; over 5 years, this saves approximately $25 billion in real PKR-equivalent debt service.

Reduced borrowing costs ($15-20B): Pakistan currently pays 1-3% premium on Eurobonds versus comparable peers; reform reduces this premium and saves approximately $15-20B over 5 years on borrowing costs.

Avoided IMF programme costs ($10-15B): If reform allows IMF programme phase-out, the next IMF programme costs (interest, conditionality, political capital) are avoided.

Inflation savings to households ($20-25B): 3-5 percent reduction in inflation premium for ~50 million working-class households at $4,000 average annual consumption.

Indirect gains ($30-60B): FDI restoration, economy formalisation tax base growth, talent retention, broader productivity effects.

Methodology caveats

These figures are projections based on comparable country experience and Pakistan-specific conditions. They are scenarios, not predictions. Actual outcomes depend on:

Implementation quality of the PCA framework

External conditions (global rates, regional stability)

Pakistani political stability through implementation

Speed of phased rollout

Compliance enforcement rigor

Industry response and operational adoption rates

Conservative scenarios produce the low-end figures ($125 billion 5-year benefit). Aggressive scenarios produce the high-end figures ($180 billion). Both ends are below what some peer-country comparisons would predict. Both ends are conservative relative to the upper-bound estimates of total Pakistani offshore wealth.

In closing

The 5-year outlook is not a guarantee. It is a scenario. The scenario is built on mechanisms that are themselves grounded in comparable country experience. The mechanisms are documented. The order of magnitude is robust to reasonable variation in the underlying assumptions.

What the outlook demonstrates is that the PCA reform is not marginal. It is transformational. The cumulative 5-year benefit of $125 to 180 billion exceeds Pakistan's current external debt. It exceeds 50 percent of current GDP. Distributed across 165 million Pakistanis, it represents a genuine economic improvement that no incremental reform of the current framework could match.

The cost of inaction is $25 to 36 billion in destroyed value annually, multiplied by every year the status quo persists. The benefit of action is $125 to 180 billion over 5 years.

The arithmetic is clear. The path forward is, as it always has been, a choice.

Thank you for reading.

, Asad Baig, Lahore, May 2026

Frequently asked questions

What is the projected Pakistani foreign reserves figure in 2031 under PCA reform? $47 to 57 billion, compared to $21.79 billion verified in March 2026. The projection is built on $25 to 35 billion in productive class repatriation, $5 to 10 billion in reduced offshore migration of ongoing flows, and $5 to 10 billion in RDA growth and diaspora savings expansion.

What is the projected USD/PKR exchange rate in 2031 under PCA reform? 200 to 225 PKR per USD, 20 to 28 percent stronger than the current rate of approximately 280. The mechanism is increased dollar supply through formal channels as productive earners route earnings through Pakistani banks instead of offshore structures.

What is the projected Pakistani inflation rate in 2031 under PCA reform? 6 to 9 percent, compared to current 12 to 15 percent. The reduction comes from stronger rupee reducing imported inflation, reduced external borrowing reducing monetary accommodation, and lower subsidy needs.

What is the cumulative 5-year benefit of PCA reform? $125 to 180 billion. Components: $25 to 35 billion in additional reserves, approximately $25 billion in reduced debt-service costs from currency strengthening, $15 to 20 billion in reduced borrowing costs from lower risk premium, $10 to 15 billion in avoided IMF programme costs, $20 to 25 billion in household inflation savings, and $30 to 60 billion in indirect gains from FDI, formalisation, and retained talent.

Will Pakistan still need IMF programmes under PCA reform? The 5-year projection has IMF programme dependence phasing out, not eliminated. Existing IMF obligations continue to be honoured. The need for new programmes reduces as reserves strengthen and external conditions improve. By 2031, Pakistan is projected to be in a position to phase out IMF programme dependence, similar to how comparable peer countries have done.

How much does the working class benefit under PCA reform? Approximately $20 to 25 billion in 5-year cumulative inflation savings, distributed across 150 million working-class Pakistani households. This is the single largest direct benefit to the largest number of beneficiaries, even though the working class never opens an FCY account.

Are the 5-year projections guaranteed? No. They are scenarios based on comparable country experience and Pakistan-specific conditions. Actual outcomes depend on implementation quality, external conditions, Pakistani political stability, speed of phased rollout, compliance enforcement rigor, and industry response. Conservative scenarios produce the low-end figures; aggressive scenarios produce the high-end figures.

How does Pakistan's IT industry growth contribute to the projection? IT exports are projected to grow from $4.5-5 billion currently to $15-20 billion by 2031. This includes both the measurement effect of bringing currently offshore-held earnings into Pakistani statistics ($0.5-3 billion immediate) and the structural growth from removing operational friction that currently constrains industry expansion (additional $10-15 billion over 5 years).

Sources

Position Paper: The Foreign Currency Account Problem in Pakistan, May 2026, Section 6

State Bank of Pakistan, Foreign Exchange Reserves Series (March 2026)

World Bank Pakistan Country Update 2025

IMF Article IV consultation reports for Pakistan

Pakistan Software Export Board, IT exports historical data

Asian Development Bank verification of 2.37 million Pakistani freelancers

Reserve Bank of India, EEFC and LRS performance data (comparator)

Bangladesh Bank, ERQ performance data (comparator)

OCCRP "Dubai Unlocked" investigation, May 2024

Atlas of Offshore World data on Pakistani offshore wealth