Why the PCA design exceeds international anti-money-laundering standards while delivering productive-class banking access

By Asad Baig · Lahore · May 2026 · Approx. 9-min read

What this cluster post is part of

This is one of four cluster posts under the Productive Capital Account: a reform proposal for Pakistan's FCY system. The companion posts are PCA eligibility, caps, and mechanics explained, Pakistan reserves 5-year outlook under PCA reform, and why FCY reform has not happened in 33 years.

This post focuses on the architecture that makes the PCA structurally safer than the current ESFCA framework while remaining FATF-compliant. The five non-negotiable safeguards. Each one closes a specific failure mode that destroyed PERA in 1998. Each one exceeds current Pakistani anti-money-laundering practice.

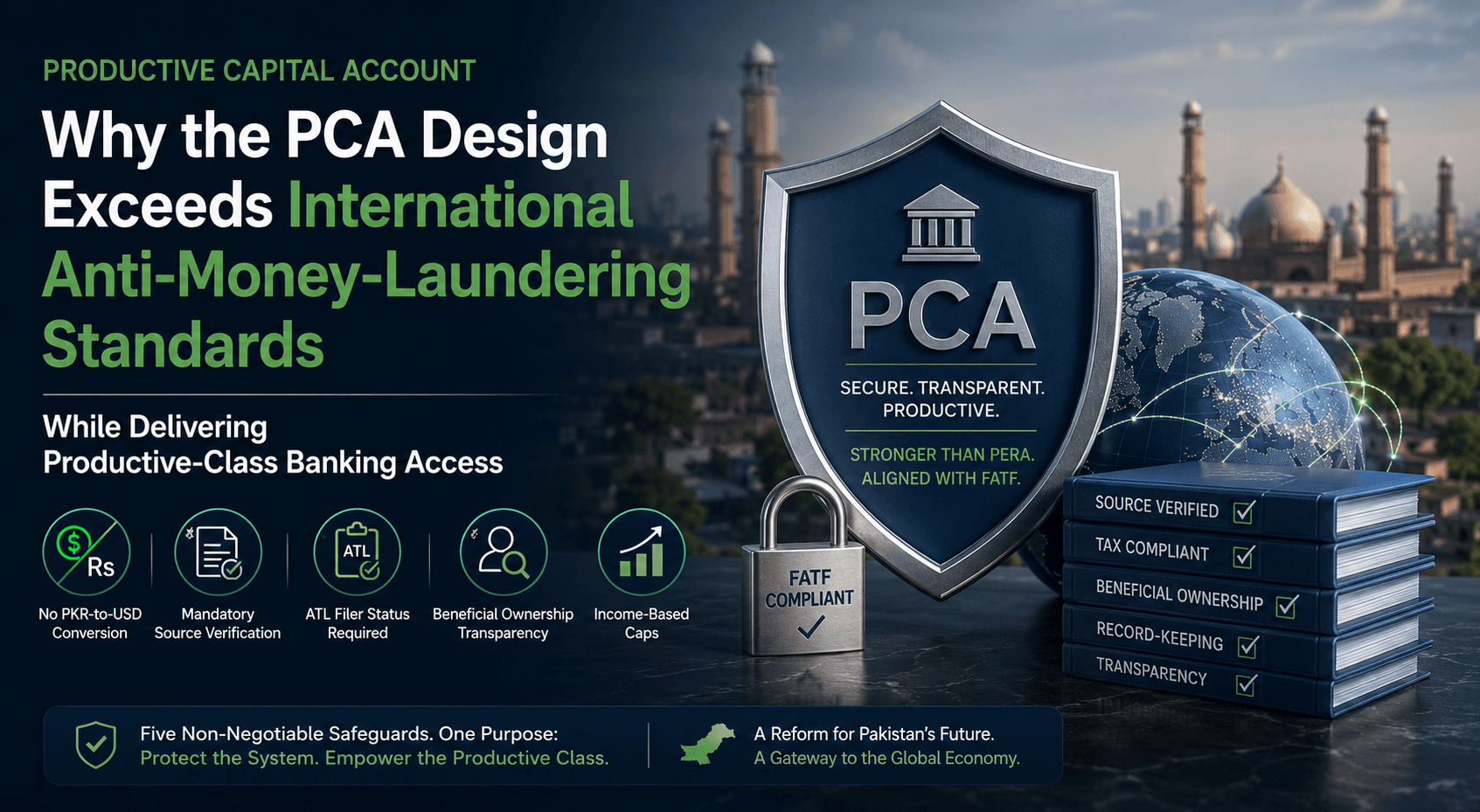

The five safeguards in one paragraph

The Productive Capital Account is built around five non-negotiable safeguards. First, no PKR-to-USD conversion permitted for deposits, eliminating the laundering pump that destroyed PERA. Second, mandatory source verification on every deposit with full documentation, exceeding current PERA Section 5 practice (which prohibits source inquiry). Third, Active Taxpayer List membership required for residents, integrating the PCA with the formal tax architecture. Fourth, beneficial ownership transparency declared at account opening and updated on changes, with cross-checking against the SECP corporate registry and NADRA-verified CNIC numbers. Fifth, income-based tiered caps preventing excessive accumulation by any single entity. Together, these safeguards exceed FATF Recommendations 10 (Customer Due Diligence) and 11 (Record-Keeping) and align with international best practices in countries that operate liberalised FCY frameworks under FATF compliance.

Safeguard 1: No PKR-to-USD conversion at deposit

This is the most important safeguard. It is also the rule that distinguishes the PCA from PERA 1992 most fundamentally.

Operationally, this means PCA accounts can only be credited via:

Inward wire transfers from foreign banks

Direct deposits from international payment processors (Stripe, PayPal, Wise, Payoneer)

Inward remittances from documented foreign employers

Foreign credit-card or merchant settlement to the account holder

PCA accounts cannot be credited via:

Conversion of PKR balances at the bank teller

Deposits of PKR cash that the bank then converts

Transfers from PKR accounts within the same bank

Any mechanism that has rupees as the source

This single rule eliminates the laundering pump that destroyed PERA. The black-money round-trip that operated through PERA's framework becomes mechanically impossible under the PCA.

Safeguard 2: Mandatory source verification

Every deposit must arrive with documentation. This is stricter than the current PERA framework, which under Section 5 explicitly prohibits inquiry into source.

The verification standards align with FATF Recommendations 10 (Customer Due Diligence) and 11 (Record-Keeping). The Pakistani Financial Monitoring Unit (FMU) integrates with the PCA framework so that suspicious patterns trigger reporting in real time.

PERA Section 5 is repealed for PCA purposes. The blanket prohibition on source inquiry that has shielded elite black money for 33 years no longer applies to PCA-routed flows. Source verification becomes the gateway to access, not an exception to it.

Safeguard 3: ATL filer status required for residents

Resident PCA holders must have Active Taxpayer List (ATL) membership and consistent annual filings with the Federal Board of Revenue. Foreign income must be declared. The PCA is not a tax shelter.

The Tax Integration

ATL membership | Required at account opening Verified continuously |

|---|---|

Annual filings | Required on time Non-filers blocked from new operations |

Foreign income declaration | Mandatory Reconciled with PCA flows |

Connection to FBR | Real-time at account level |

This safeguard accomplishes two things simultaneously. It excludes the parallel-economy operators who could otherwise abuse the framework. And it directly increases tax filing among productive earners, because PCA access becomes a strong incentive to maintain ATL status. Pakistan's ATL membership has stagnated for years. The PCA framework would push it upward.

Non-filers cannot open PCA accounts. Filers who fall off the ATL must remediate before continuing PCA operations. The integration with FBR ATL checking is automatic at the bank's onboarding system.

Safeguard 4: Beneficial ownership transparency

Ultimate beneficial owners must be declared at account opening, updated within 30 days of any change, and cross-checked against the SECP corporate registry.

Beneficial Ownership Standards

For natural persons | Holder is the owner |

|---|---|

For Pakistani companies | UBO any natural person owning 10%+; declared with NADRA-verified CNIC numbers |

For trusts and partnerships | Full beneficiary disclosure |

For foreign entities | Cross-jurisdictional UBO disclosure required |

Updates | Within 30 days of any change |

This safeguard closes the front-men loophole that has historically been used to feed FCY accounts of influential people through nominee structures. Under the PCA, a nominee structure is an immediate red flag triggering enhanced due diligence and possible account closure.

The integration with the SECP corporate registry and NADRA's CNIC verification system provides operational rigour. Beneficial ownership claims that contradict registry data trigger automatic review. Updates are mandatory and tracked.

Safeguard 5: Income-based caps on accumulation

Tiered caps prevent excessive accumulation by any single entity while permitting productive operations. The cap design is calibrated to actual earnings.

The Cap Structure

Verified freelancer | Up to $200,000 per year |

|---|---|

IT company (PSEB) | Up to 100% declared FX |

Goods/service exporter | Up to 100% declared FX |

Resident professional | Up to $250,000 per year |

Importer (operational) | Up to 12-month historical import requirement |

Overseas Pakistani | Current RDA caps + expansion |

The cap structure ensures that no single account becomes a vehicle for moving sums disproportionate to legitimate earnings. It also ensures that the PCA cannot be used as a vault for non-operational accumulation by one entity at the expense of access for others.

For IT companies, goods exporters, and service exporters, the cap is set at 100 percent of declared foreign exchange earnings, which automatically grows with the business. For freelancers and resident professionals, fixed dollar caps prevent disproportionate accumulation. For importers, the cap is sized to operational requirement.

For the detailed cap mechanics by category, see PCA eligibility, caps, and mechanics explained.

Why these five safeguards exceed FATF standards

FATF Recommendation 10 requires customer due diligence including identification, verification, beneficial ownership identification, ongoing monitoring, and risk-based approach. FATF Recommendation 11 requires record-keeping for at least five years.

PCA Safeguards Vs FATF Minimums

FATF requires | PCA delivers |

|---|---|

Customer identification | NADRA-verified CNIC, biometric where applicable |

Beneficial ownership | Declared at opening, updated |

identification | within 30 days |

Source-of-funds | Documentation per deposit; |

verification | stricter than current PERA practice |

Ongoing monitoring | FMU integration; real-time pattern detection |

Risk-based approach | Tiered caps + sector-specific verification |

Record-keeping | Mandatory beyond 5 years |

The PCA exceeds each FATF minimum. The framework's compliance is not designed to barely satisfy FATF. It is designed to be FATF-best-in-class while delivering productive-class banking access.

This is what India, Singapore, UAE, Malaysia, and Bangladesh have in common: they all operate liberal productive-class FCY access alongside compliance regimes that exceed FATF minimums. Compliance and access are complements in their frameworks, not opposites.

For the international comparison evidence, see what India, Singapore, UAE, Malaysia and Bangladesh do that Pakistan refuses to.

Why these safeguards prevent the 1998 mechanism

Each safeguard addresses a specific PERA failure mode:

Pera → Pca: How Safeguards Prevent The 1998 Mechanism

PERA 1998 failure | PCA prevention |

|---|---|

Unlimited PKR→USD | Safeguard 1: only foreign- source USD accepted |

No source verification | Safeguard 2: mandatory per- deposit verification |

No tax integration | Safeguard 3: ATL filer status required for residents |

No beneficial ownership | Safeguard 4: UBO declared and updated continuously |

Unlimited accumulation | Safeguard 5: income-based tiered caps |

Liability mismatch w/ | Real FX assets back FX |

reserves | liabilities (no PKR- denominated convertibles) |

The PCA holdings are real foreign currency. The dollars in PCA accounts arrived as dollars and remain as dollars. The bank's internal Asset-Liability Management ensures FX assets match FX liabilities. There is no mechanism by which a panic event could produce a 1998-style freeze, because there is no liability mismatch to expose.

For the broader analysis of how the 1998 freeze worked and why the PCA structurally cannot repeat it, see the 1992 Protection of Economic Reforms Act: PERA explained and May 28, 1998: the day Pakistan froze all foreign currency accounts.

In closing

The five safeguards are the architecture that makes the rest of the PCA framework safe. Without them, the PCA collapses into PERA. With them, the PCA is a strictly compliant productive-economy banking framework that exceeds international best practices.

The safeguards are also what distinguishes honest reform from the various "reform theatre" gestures of the past decade. Form R elimination, retention rate adjustments, and SBP circular updates are operational tweaks. The five safeguards are structural changes that close the specific failure modes Pakistan has lived through.

Any reform proposal that does not include all five safeguards is not the PCA. Any reform that includes all five is, in the most important sense, the PCA, regardless of what name it operates under. The architecture is the proposal. The label is secondary.

Thank you for reading.

, Asad Baig, Lahore, May 2026

Frequently asked questions

What are the five non-negotiable safeguards of the Productive Capital Account? First, no PKR-to-USD conversion permitted for deposits. Second, mandatory source verification on every deposit. Third, Active Taxpayer List status required for residents. Fourth, beneficial ownership transparency declared at opening with updates on changes. Fifth, income-based tiered caps on accumulation calibrated to actual earnings.

Why is "no PKR-to-USD conversion at deposit" the most important safeguard? Because this single rule eliminates the laundering pump that destroyed PERA in 1998. PERA allowed unlimited PKR-to-USD conversion, creating USD liabilities backed by PKR convertible balances; the SBP could not honour these in actual USD when demand spiked. The PCA closes this mechanism by accepting only foreign-source dollars at the deposit point.

Does the PCA require source verification? Yes. Every PCA deposit must arrive with documentation: wire transfer record, foreign client invoice, platform earnings statement, foreign employer payslip, or foreign credit-card or merchant settlement. This exceeds the current PERA Section 5 framework, which prohibits inquiry into the source of foreign currency deposits.

Is ATL filer status required for the PCA? Yes, for resident holders. PCA holders must have Active Taxpayer List membership and consistent annual filings with the Federal Board of Revenue. Foreign income must be declared. Non-filers cannot open PCA accounts. The integration with FBR ATL checking is automatic at the bank's onboarding system.

How does the PCA verify beneficial ownership? Ultimate beneficial owners are declared at account opening, updated within 30 days of any change, and cross-checked against the SECP corporate registry. For Pakistani companies, any natural person owning 10 percent or more must be declared with NADRA-verified CNIC numbers. For trusts and partnerships, full beneficiary disclosure is required. Nominee structures trigger enhanced due diligence and possible account closure.

What are the income-based caps under the PCA? For freelancers, up to $200,000 per year. For IT companies (PSEB-registered), up to 100 percent of declared FX earnings. For goods and service exporters, up to 100 percent of declared FX earnings. For resident professionals, up to $250,000 per year. For importers, sized to 12-month historical import requirement. For overseas Pakistanis, current RDA caps with expansion.

Do the PCA safeguards exceed FATF standards? Yes. FATF Recommendations 10 (Customer Due Diligence) and 11 (Record-Keeping) set minimum standards. The PCA design exceeds each minimum: NADRA-verified identification, beneficial ownership declared at opening with continuous updates, source verification per deposit (stricter than current PERA practice), FMU integration for real-time pattern detection, tiered caps with sector-specific verification, and record-keeping beyond the five-year FATF minimum.

How do the safeguards prevent a repeat of the 1998 freeze? Each safeguard addresses a specific PERA failure mode. Safeguard 1 prevents the unlimited PKR-to-USD conversion that created liabilities the SBP could not back. Safeguard 2 closes the source-inquiry prohibition that enabled black-money round-tripping. Safeguard 3 integrates the framework with formal tax architecture. Safeguard 4 closes the front-men loophole. Safeguard 5 prevents disproportionate accumulation. The combined effect is that no liability mismatch exists for a panic event to expose.

Sources

Position Paper: The Foreign Currency Account Problem in Pakistan, May 2026, Section 4

FATF Recommendations 10 (Customer Due Diligence) and 11 (Record-Keeping)

FATF country mutual evaluation reports for India, Singapore, UAE, Malaysia, Bangladesh, Pakistan

Pakistan Securities and Exchange Commission, beneficial ownership regulations

NADRA verification system documentation

Federal Board of Revenue, Active Taxpayer List requirements

State Bank of Pakistan, Financial Monitoring Unit operational guidelines

Reserve Bank of India, EEFC compliance standards

Bangladesh Bank, ERQ compliance standards