How a country with comparable constraints built a substantially better foreign currency framework

By Asad Baig · Lahore · May 2026 · Approx. 9-min read

What this cluster post is part of

This is one of four cluster posts under what India, Singapore, UAE, Malaysia and Bangladesh do that Pakistan refuses to. The companion posts are India's liberalised foreign currency framework explained, Singapore, UAE and Malaysia: three FCY models Pakistan has refused to adopt, and the "currency will crash" argument: why it does not apply to verified earner reform.

This post focuses on the most uncomfortable comparison Pakistan has. Bangladesh. A country with comparable economic constraints, comparable political instability, comparable IMF programme history, and substantially better foreign currency framework outcomes for its productive class.

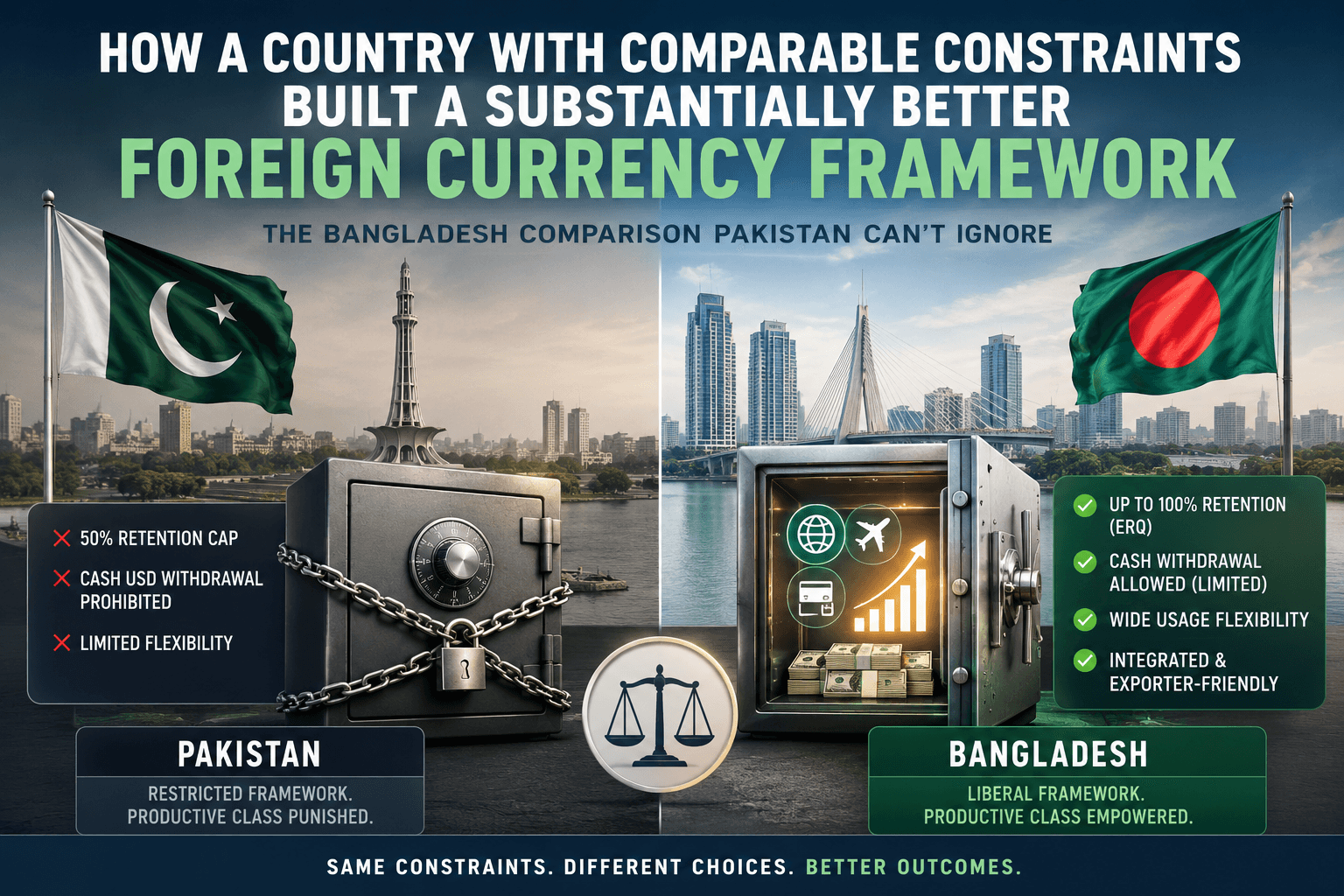

The comparison in one paragraph

Bangladesh shares almost every constraint Pakistani policymakers cite as reasons reform is impossible: developing economy status, multiple IMF programmes (current $4.7 billion), comparable political instability, FATF compliance, and similar reserve adequacy challenges. Yet Bangladesh operates an Exporter's Retention Quota (ERQ) account that allows up to 100 percent retention of export earnings depending on sector and purpose, while Pakistan's ESFCA is capped at 50 percent for IT exporters and 35 percent for general service exporters. Bangladesh allows ERQ holders to use funds for international payments, foreign travel, and operational expenses; Pakistan's ESFCA prohibits cash USD withdrawal within Pakistan. Bangladesh's IT industry has grown faster than Pakistan's in part because Bangladeshi IT entrepreneurs are not punished for repatriating their earnings. The comparison strips the pretence from arguments that productive-class FCY access requires structural conditions Pakistan lacks.

The structural comparison

Pakistan Vs Bangladesh, Structural Comparison

Pakistan | Bangladesh |

|---|---|

~$1,600 | ~$2,800 |

~240M | ~170M |

Compliant | Compliant |

Multiple | Multiple |

$7B EFF | $4.7B |

$21.79B | ~$20B |

IT, textiles | Garment, IT |

✗ Limited | ✓ Liberal |

50% (with caps) | Up to 100% (ERQ) |

No | Yes |

Limited | More liberal |

Prohibited | Limited but allowed |

The structural conditions are similar. The outcomes are different. The variable that produces different outcomes is not external constraint but internal policy choice.

What Bangladesh's ERQ allows

The Exporter's Retention Quota (ERQ) account in Bangladesh allows up to 100 percent retention of export earnings depending on sector and purpose. The framework provides:

Multi-currency holdings (USD, GBP, EUR, JPY)

Use of funds for international payments to foreign vendors

Use of funds for foreign travel related to business

Operational expense payments abroad

Foreign investment within prescribed limits

Direct integration with international payment processors

More flexible cash withdrawal than Pakistan permits

The contrast with Pakistan's ESFCA is substantial. Pakistani IT exporters retain 50 percent (with $5,000 per month minimum). Bangladeshi exporters can retain up to 100 percent. Pakistani ESFCA prohibits cash USD withdrawal within Pakistan. Bangladeshi ERQ permits limited cash withdrawal for documented purposes.

For the detailed mechanics of Pakistani ESFCA, see ESFCA explained: why 50 percent retention is bookkeeping, not banking.

Why Bangladesh's IT industry has grown faster

Bangladesh's IT industry has grown faster than Pakistan's in part because Bangladeshi IT entrepreneurs are not punished for repatriating their earnings.

Bangladesh It Industry, Recent Growth

IT exports (2024) | $1.5+ billion |

|---|---|

Year-over-year growth (recent) | 20%+ in good years |

Government support | Active courting |

Banking flexibility | ERQ + integration |

Tax incentives | IT-specific |

Special economic zones | IT-focused (HTPs) |

The Bangladesh government actively courts IT exporters with banking flexibility, tax incentives, and regulatory support. The Bangladesh IT industry crossed $1.5 billion in 2024, a smaller absolute number than Pakistan's $4.5 to 5 billion, but growing from a smaller base and with more aggressive government support.

The comparative IT growth is not the only relevant indicator. The structural factor is that Bangladeshi IT companies have less reason to maintain offshore structures because the formal Bangladeshi banking system serves their needs adequately. Pakistani IT companies route a substantial portion of earnings through Wyoming, Estonia, UAE, and other offshore jurisdictions because the formal Pakistani system does not.

The shared constraints, different choices

Bangladesh and Pakistan operate under nearly identical structural constraints:

Both are FATF-compliant

Both have current IMF programmes ($7 billion for Pakistan, $4.7 billion for Bangladesh)

Both face periodic balance-of-payments stress

Both have ~$20 billion in foreign reserves

Both have garment and textile-driven export profiles (Bangladesh more so)

Both have growing IT sectors

Both have political instability cycles

Both have comparable diaspora populations sending remittances

The constraints are similar. What is different is the framework choice.

Same Constraints, Different Choices

Constraint | PK choice | BD choice |

|---|---|---|

FATF compliance | Compliance + | Compliance + |

small-user | productive | |

friction | access | |

IMF programme | Restriction | Productive |

maintained | framework maintained | |

Reserve adequacy | Forced | Limited |

conversion | conversion | |

Capital flight risk | Restrict | Verify and |

productive class | permit | |

Diaspora savings | RDA only | ERQ + diaspora options |

The Pakistani choices have produced an estimated $25 to 36 billion in annually destroyed value (see how Pakistan's FCY system costs the productive class $25 to 36 billion a year). The Bangladeshi choices have produced a productive-class banking framework that, while not perfect, serves the productive class meaningfully better than Pakistan's framework does.

Why this comparison is uncomfortable

When Pakistani policymakers say liberalisation is impossible because of FATF or IMF rules, the simplest counter-argument is: Bangladesh does it. Bangladesh shares almost every Pakistani constraint and has more liberal productive-class FCY access. The argument that Pakistan cannot do what Bangladesh does because of constraints they share is internally inconsistent.

The Pakistani argument has historically been:

"FATF won't let us liberalise", Bangladesh is FATF-compliant with ERQ

"IMF won't let us liberalise", Bangladesh runs an IMF programme with ERQ

"Reserves are too low", Bangladesh has comparable reserves and operates ERQ

"Capital flight risk is too high", Bangladesh manages this through verification, not exclusion

"Political instability prevents reform", Bangladesh has comparable instability

Each Pakistani constraint that supposedly prevents reform is a constraint Bangladesh shares and has nonetheless reformed under. The variable producing different outcomes is not external. It is domestic political will.

What Pakistan should be demanding

If Pakistan wants the most direct, peer-comparable evidence that productive-class FCY reform is feasible without destabilising the country, Bangladesh is that evidence.

The Productive Capital Account proposal is closer to the Bangladesh ERQ model than to any other comparable framework. The PCA's 100 percent retention for IT exporters mirrors ERQ's sector-based 100 percent retention. The PCA's permission for foreign payments mirrors ERQ operational practice. The PCA's source verification, beneficial ownership, and tax-filer requirements exceed ERQ standards while remaining FATF-compliant.

For the full PCA design, see the Productive Capital Account: a reform proposal for Pakistan's FCY system. For the broader international comparison, see what India, Singapore, UAE, Malaysia and Bangladesh do that Pakistan refuses to.

In closing

Bangladesh is the comparison Pakistan most needs and most avoids. The avoidance is understandable. The comparison is uncomfortable because it demonstrates that Pakistan's chosen framework is the result of internal political economy, not external constraint.

The next time a Pakistani policymaker, banker, or commentator argues that productive-class FCY reform is impossible because of structural conditions, the question to ask is simple: how does Bangladesh do it? If Bangladesh does it under conditions comparable to Pakistan's, what is the actual obstacle in Pakistan?

The actual obstacle, as I have argued throughout this series, is the political organisation of the 200,000 Pakistani beneficiaries of the current framework against the 165 million Pakistani potential beneficiaries of reform. The math changes only when the dispersed organise. Bangladesh's example is one of the strongest pieces of evidence available to that organising effort.

Thank you for reading.

, Asad Baig, Lahore, May 2026

Frequently asked questions

What is Bangladesh's Exporter's Retention Quota (ERQ) account? The ERQ account in Bangladesh allows exporters to retain up to 100 percent of their foreign exchange earnings in foreign currency, depending on sector and purpose. The funds can be used for international payments to foreign vendors, foreign travel for business purposes, operational expenses abroad, and limited foreign investment. The framework supports multi-currency holdings.

How does Bangladesh's ERQ compare to Pakistan's ESFCA? Bangladesh's ERQ allows up to 100 percent retention. Pakistan's ESFCA caps retention at 50 percent for IT exporters and 35 percent for general service exporters. Bangladesh permits limited cash withdrawal of foreign currency for documented purposes; Pakistan prohibits cash USD withdrawal from ESFCA within Pakistan. Bangladesh has more flexible operational use of retained funds.

Is Bangladesh FATF-compliant? Yes. Bangladesh is FATF-compliant under the same FATF standards Pakistan must meet. Bangladesh operates the ERQ framework alongside this compliance, demonstrating that productive-class FCY access and FATF compliance are compatible.

Does Bangladesh have an IMF programme? Yes. Bangladesh has a current $4.7 billion IMF programme as of 2024. The IMF programme is compatible with the ERQ framework, demonstrating that IMF compatibility does not require restrictive productive-class FCY access.

Why has Bangladesh's IT industry grown faster than Pakistan's recently? Bangladesh's IT industry has grown faster in part because Bangladeshi IT entrepreneurs are not punished for repatriating their earnings. The Bangladesh government actively courts IT exporters with banking flexibility, tax incentives, and regulatory support. Bangladeshi IT companies have less reason to maintain offshore structures because the formal Bangladeshi banking system serves their needs better than Pakistan's serves Pakistani equivalents.

What is the structural similarity between Pakistan and Bangladesh? Both are FATF-compliant, both have current IMF programmes, both face periodic balance-of-payments stress, both have approximately $20 billion in foreign reserves, both have garment and textile-driven export profiles, both have growing IT sectors, both have political instability cycles, and both have comparable diaspora populations sending remittances.

What does the Bangladesh comparison demonstrate for Pakistan? That productive-class FCY reform is feasible under conditions comparable to Pakistan's. The Pakistani argument that reform is impossible due to FATF, IMF, reserves, or political instability constraints fails when applied to Bangladesh, which has the same constraints and has nonetheless built a more productive framework. The variable producing different outcomes is domestic political will, not external constraint.

How does the Productive Capital Account compare to Bangladesh's ERQ? The PCA is closer to the ERQ model than to any other comparable framework. The PCA's 100 percent retention for IT exporters mirrors ERQ's sector-based retention. The PCA's permission for documented foreign payments mirrors ERQ operational practice. The PCA's source verification, beneficial ownership transparency, and tax-filer requirements exceed ERQ compliance standards while remaining FATF-compliant.

Sources

Bangladesh Bank, Foreign Exchange Regulations and ERQ guidelines

World Bank Bangladesh Development Update 2024

IMF Article IV consultation reports for Pakistan and Bangladesh

FATF country mutual evaluation reports for Pakistan and Bangladesh

Bangladesh IT exports data (2024)

Pakistan IT exports data: SBP and Pakistan Software Export Board, FY2025-26 figures

Position Paper: The Foreign Currency Account Problem in Pakistan, May 2026

Related reading

What India, Singapore, UAE, Malaysia and Bangladesh Do That Pakistan Refuses To

Singapore, UAE and Malaysia: Three FCY Models Pakistan Has Refused to Adopt

The "Currency Will Crash" Argument: Why It Does Not Apply to Verified Earner Reform

The Productive Capital Account: A Reform Proposal for Pakistan's FCY System

ESFCA Explained: Why 50% Retention Is Bookkeeping, Not Banking