The non-negotiable architecture that prevents the 1998 mechanism while exceeding FATF standards

By Asad Baig · Lahore · May 2026 · Approx. 4-min read

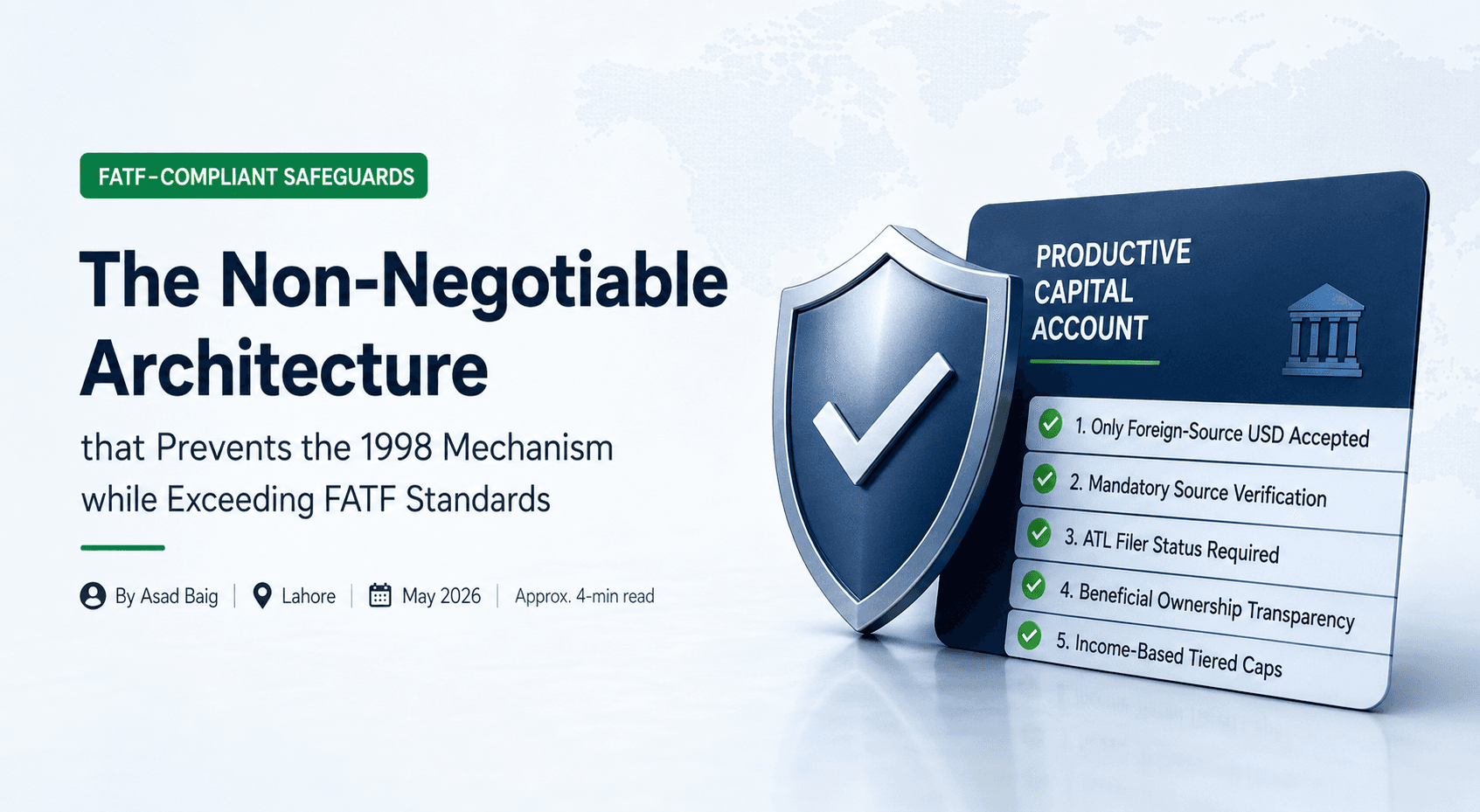

The short answer

The Productive Capital Account has five non-negotiable safeguards. (1) No PKR-to-USD conversion permitted for deposits, eliminates the laundering pump that destroyed PERA. (2) Mandatory source verification on every deposit, stricter than current PERA Section 5 practice. (3) ATL filer status required for residents, integration with formal tax architecture. (4) Beneficial ownership transparency declared at opening with updates, closes the front-men loophole. (5) Income-based tiered caps, prevents disproportionate accumulation. Each safeguard addresses a specific PERA failure mode, and together they exceed FATF Recommendations 10 and 11.

This is a Tier 3 long-tail spoke under the five FATF-compliant safeguards of the Productive Capital Account.

The five safeguards mapped to PERA failure modes

Each Safeguard Closes A Pera Failure Mode

PERA failure | PCA safeguard |

|---|---|

Unlimited PKR→USD | #1: Only foreign-source USD accepted |

No source verification | #2: Mandatory verification per deposit |

No tax integration | #3: ATL filer status required |

No beneficial ownership | #4: UBO declared and updated continuously |

Unlimited accumulation | #5: Income-based tiered caps |

Each PERA failure that produced the 1998 catastrophe is structurally prevented in the PCA design. The PCA cannot repeat the 1998 mechanism because the mechanism has been engineered out.

How the safeguards exceed FATF standards

FATF Rec 10 (Customer Due Diligence): PCA exceeds via NADRA-verified CNIC, beneficial ownership at opening, ongoing monitoring through FMU

FATF Rec 11 (Record-Keeping): PCA exceeds via mandatory record retention beyond 5-year minimum

Source verification: stricter than current Pakistani practice

Risk-based approach: tiered caps + sector-specific verification

Ongoing monitoring: real-time pattern detection through FMU integration

The compliance is integrated into the operational design, not added as an afterthought. This is the same approach Singapore, UAE, India, Malaysia, and Bangladesh take in their respective frameworks.

Frequently asked questions

What is the most important PCA safeguard? Safeguard 1: no PKR-to-USD conversion permitted for deposits. This single rule eliminates the laundering pump that destroyed PERA in 1998. It is what makes the PCA structurally different from PERA.

How does the PCA verify source of funds? Every deposit requires documentation: wire transfer record with foreign payer details, foreign client invoice with corporate identity, platform earnings statement, foreign employer payslip, or foreign credit card or merchant settlement statement. This exceeds the current PERA Section 5 framework, which prohibits source inquiry.

What does ATL filer status mean for the PCA? Resident PCA holders must have Active Taxpayer List membership and consistent annual filings with the FBR. Foreign income must be declared. Non-filers cannot open PCA accounts. The integration with FBR ATL checking is automatic at the bank's onboarding system.

How does the PCA verify beneficial ownership? Ultimate beneficial owners declared at account opening, updated within 30 days of any change, cross-checked against the SECP corporate registry. For Pakistani companies, any natural person owning 10 percent or more must be declared with NADRA-verified CNIC numbers. Nominee structures trigger enhanced due diligence.

What are the income-based caps? For freelancers, up to $200,000/year. For IT companies (PSEB), up to 100% of declared FX. For goods/service exporters, up to 100% of declared FX. For resident professionals, up to $250,000/year. For importers, sized to 12-month historical import requirement.

Does the PCA exceed FATF requirements? Yes. The PCA exceeds FATF Recommendations 10 (Customer Due Diligence) and 11 (Record-Keeping) through NADRA-verified identification, beneficial ownership at opening with continuous updates, source verification per deposit, FMU integration for real-time pattern detection, tiered caps, and record-keeping beyond the 5-year FATF minimum.

Sources

Position Paper: The Foreign Currency Account Problem in Pakistan, May 2026, Section 4

FATF Recommendations 10 and 11

Pakistan SECP beneficial ownership regulations

NADRA verification system documentation

FBR ATL requirements