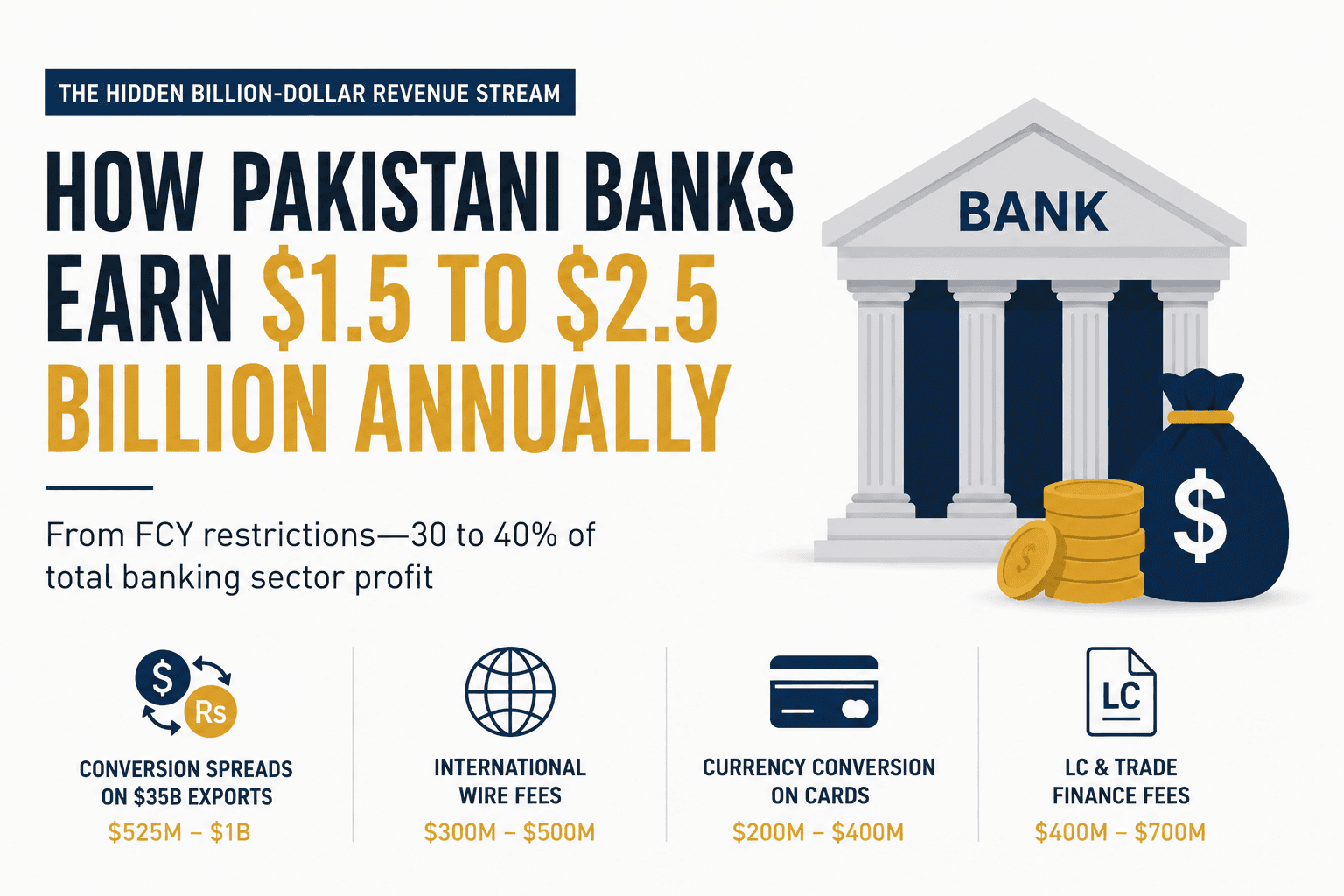

$1.5 to 2.5 billion annually, approximately 30 to 40 percent of total banking sector profit

By Asad Baig · Lahore · May 2026 · Approx. 5-min read

The short answer

Pakistani banks earn approximately $1.5 to 2.5 billion annually from FCY restriction-related fees and spreads. This represents approximately 30 to 40 percent of total Pakistani banking sector profit. The top five Pakistani banks (HBL, MCB, UBL, NBP, Bank Alfalah) collectively report approximately PKR 600 to 700 billion (about $2.1 to 2.5 billion) in annual profits, of which the FCY-related portion is the largest single component.

This is a Tier 3 long-tail spoke under why your Pakistani bank card charges 25 to 40 percent on Facebook ads and parent pillar how Pakistan's FCY system costs the productive class $25 to 36 billion a year.

Revenue breakdown

Pakistani Banks' Fcy Restriction Revenue

Source | Annual revenue |

|---|---|

Conversion spreads on $35B exports | $525M - $1B |

International wire transfer fees | $300M - $500M |

Currency conversion on cards | $200M - $400M |

LC and trade finance fees | $400M - $700M |

TOTAL BANKING REVENUE FROM FCY | $1.5B - $2.5B |

This revenue stream is one of the most reliable in Pakistani banking. It does not depend on macroeconomic cycles. It does not depend on credit quality. It depends only on the FCY framework remaining restrictive enough to require banks to play their gatekeeping role on every export receipt and every international payment.

Top Pakistani banks by 2024 profit

Top Pakistani Banks, 2024 Approximate Profit

Bank | Annual profit |

|---|---|

Habib Bank Limited (HBL) | ~PKR 80 billion |

MCB Bank | ~PKR 75 billion |

United Bank Limited (UBL) | ~PKR 70 billion |

National Bank of Pakistan (NBP) | ~PKR 50 billion |

Bank Alfalah | ~PKR 45 billion |

Combined banking sector profit | ~PKR 600-700 billion (~$2.1-2.5 billion) |

The FCY restriction-related portion is approximately $1.5 to 2.5 billion of this total. Reform that eliminates the framework would reduce banking sector profitability significantly. This is the structural reason banks have political incentive to defend the current framework.

The bank-government symbiosis

Pakistani banks and the government operate in a symbiotic relationship that makes reform politically difficult:

Banks give the government massive loans to finance budget deficits

Banks hold government securities at favourable rates

Banks pay tax revenue (heavily taxed but pass costs to customers)

Banks comply with government priorities (lending directives)

Banks receive a restrictive FCY framework that maintains profit margins

Banks receive interest rate spreads protected through SBP policy

Banks receive bailouts when needed (NPL forgiveness, recapitalisation)

Banks receive regulatory protection from new competition

This is why the banking sector cannot reform itself. It is captured. It cannot be the agent of its own reform because its profits depend on the framework continuing.

Frequently asked questions

How much do Pakistani banks earn annually from FCY restrictions? Approximately $1.5 to 2.5 billion, representing 30 to 40 percent of total Pakistani banking sector profit. Sources include conversion spreads on $35 billion in exports ($525 million to $1 billion), international wire transfer fees ($300 to 500 million), currency conversion on cards ($200 to 400 million), and LC and trade finance fees ($400 to 700 million).

What is the total profit of Pakistani banks? Approximately PKR 600 to 700 billion ($2.1 to 2.5 billion) annually for the combined banking sector. Top five banks: HBL ~PKR 80 billion, MCB ~PKR 75 billion, UBL ~PKR 70 billion, NBP ~PKR 50 billion, Bank Alfalah ~PKR 45 billion.

What percentage of Pakistani banking profits comes from FCY restrictions? Approximately 30 to 40 percent. This is one of the most reliable revenue streams in Pakistani banking and does not depend on macroeconomic cycles or credit quality.

Why won't Pakistani banks support FCY reform? Reform would reduce banking sector profitability significantly. The FCY restriction-related revenue would be lost or reduced under fundamental reform. The banking sector is structurally aligned with the current framework rather than with reform proposals.

Do Pakistani banks have political influence over FCY policy? Yes. Pakistani banks operate in a symbiotic relationship with the government, lending massively to finance budget deficits, holding government securities, and providing infrastructure. In exchange, they receive a restrictive FCY framework that maintains profit margins. The Pakistan Banks' Association is one of the most politically connected industry bodies in the country.

Would the Productive Capital Account eliminate this revenue stream? Partially. The PCA would eliminate the largest portion (forced conversion spreads on IT exports, international wire fees, card markup) while preserving banking revenue from legitimate operational fees on PCA-routed transactions. The net effect is a substantial reduction in FCY-restriction revenue but not its elimination.

Sources

2024 Pakistani banking sector profit data (HBL, MCB, UBL, NBP, Bank Alfalah)

State Bank of Pakistan, banking sector profitability statistics

Pakistan Banks' Association policy positions

Position Paper: The Foreign Currency Account Problem in Pakistan, May 2026