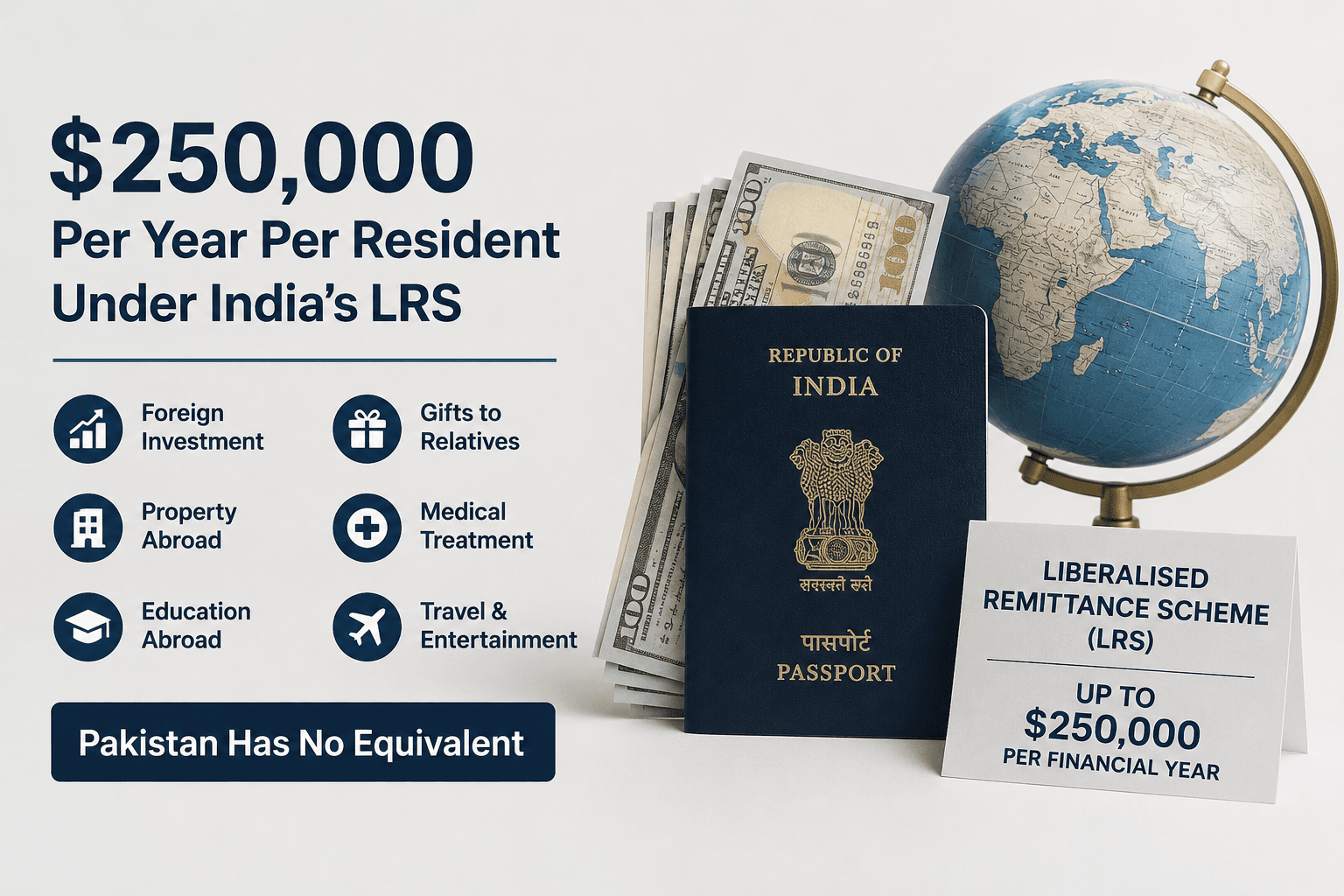

$250,000 per year per resident for foreign investment, property, education, and gifts, Pakistan has nothing equivalent

By Asad Baig · Lahore · May 2026 · Approx. 4-min read

The short answer

The Liberalised Remittance Scheme (LRS) is a Reserve Bank of India scheme that allows any Indian resident to remit up to $250,000 per financial year for any permitted current or capital account transaction, including foreign investment, property purchases, gifting to relatives abroad, education abroad, medical treatment abroad, maintenance of relatives abroad, and travel and entertainment. There is no project-by-project approval process. The remittance happens through a designated Authorised Dealer bank with a simple declaration. Pakistani citizens have nothing equivalent.

This is a Tier 3 long-tail spoke under India's liberalised foreign currency framework explained.

What LRS allows

The LRS operates without project-by-project approval. An Indian resident chooses how to use the $250,000 limit each year. The bank processes the remittance through a simple declaration that the resident is using their LRS quota.

Pakistan has no equivalent

Pakistani citizens cannot remit $250,000 per year freely for foreign investment, property purchase, education, or gifts. The closest Pakistani approximation requires project-by-project SBP approval with substantial documentation, branch officer discretion, and unpredictable processing.

The current Pakistani framework on outward remittance for individuals is restrictive. Specific allowances exist (limited travel allowance, limited education remittance, limited medical remittance) but each requires documentation and approval. There is no framework comparable to LRS that allows the resident to choose how to use a defined annual quota.

The political-economic gap

The LRS exists in India because the political constituency for productive-class FCY access has been organized for decades. The LRS does not exist in Pakistan because the same constituency has not been comparably organized.

For the analysis of why Pakistani productive class organization matters, see why FCY reform has not happened in 33 years and why the productive class must organise.

Frequently asked questions

What is India's Liberalised Remittance Scheme? A Reserve Bank of India scheme allowing any Indian resident to remit up to $250,000 per financial year for any permitted current or capital account transaction, with no project-by-project approval, through a designated Authorised Dealer bank.

What is the LRS annual limit per Indian resident? $250,000 per financial year. The limit applies per individual resident.

What can LRS remittances be used for? Foreign investment (stocks, bonds, real estate), buying foreign property, gifting to relatives abroad, education abroad, medical treatment abroad, maintenance of relatives abroad, and travel and entertainment.

Does Pakistan have an equivalent of LRS? No. Pakistani citizens cannot remit comparable amounts annually without project-by-project SBP approval. The closest Pakistani approximation requires substantial documentation, branch officer discretion, and unpredictable processing for each remittance.

Is the LRS FATF-compliant? Yes. The LRS operates alongside India's FATF compliance and IMF programmes. Source verification, KYC, and beneficial ownership tracking are integrated into the LRS process.

Why does India have LRS and Pakistan does not? Because the political constituency for productive-class FCY access has been organized in India for decades. The same constituency has not been comparably organized in Pakistan, where the political math has favoured the 200,000 organized beneficiaries of the current restrictive framework against the 165 million atomized potential reform beneficiaries.

Sources

Reserve Bank of India, Liberalised Remittance Scheme regulations

RBI Master Direction on Foreign Exchange Management

Position Paper: The Foreign Currency Account Problem in Pakistan, May 2026