A direct answer with the legal text effect, the dollar estimate, and what reform requires

By Asad Baig · Lahore · May 2026 · Approx. 5-min read

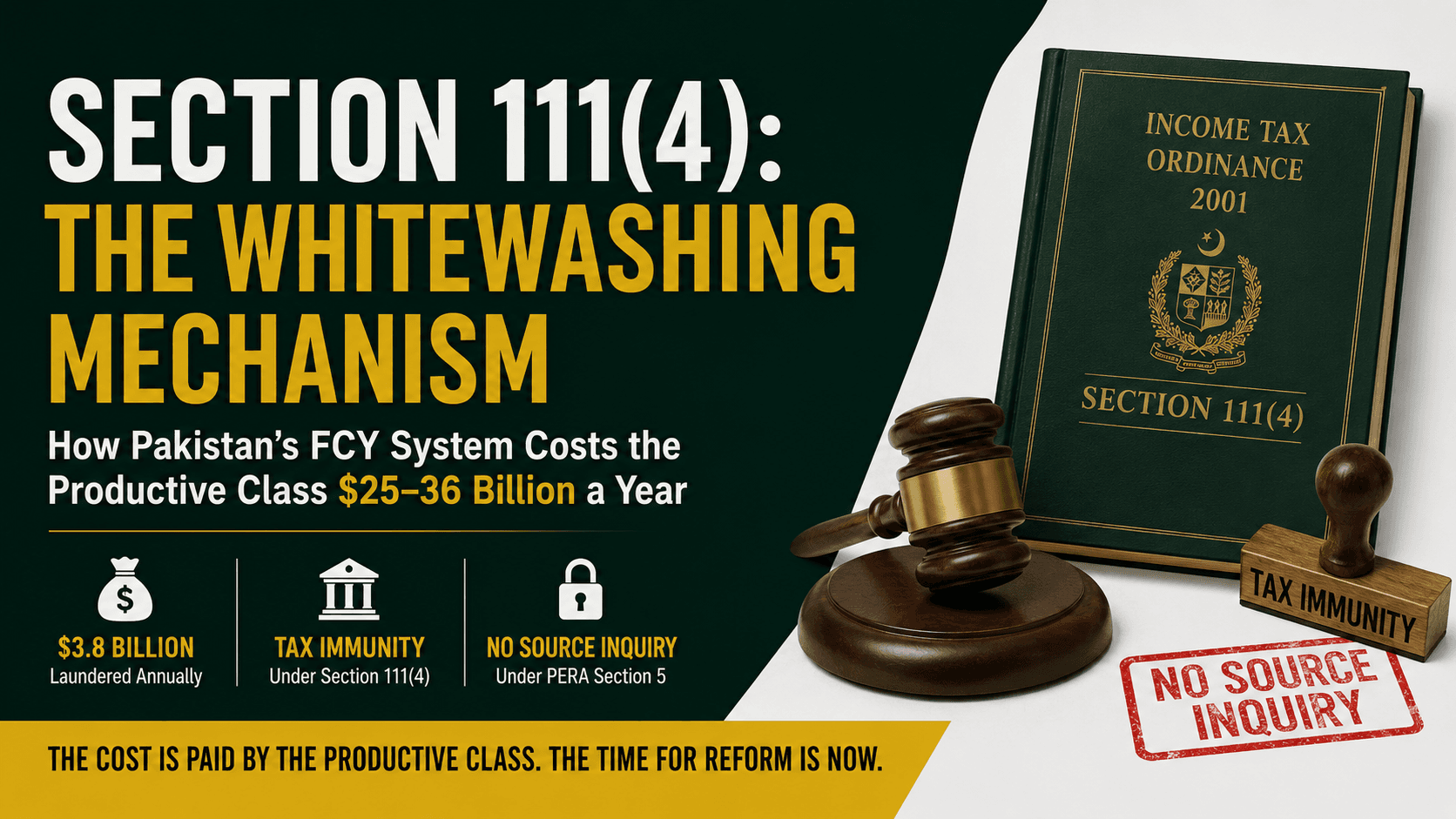

The short answer

Section 111(4) of Pakistan's Income Tax Ordinance grants tax immunity to inward foreign remittances regardless of source. It prevents the Federal Board of Revenue from inquiring into the source of any foreign remittance received through formal banking channels. Combined with PERA Section 5, which prohibits source inquiry on foreign currency deposits, it creates a legal corridor for whitewashing domestically generated black money. A 2018 tax compliance analysis estimated approximately $3.8 billion a year is whitewashed through this single mechanism.

This is a Tier 3 long-tail spoke under Section 111(4) of Pakistan's Income Tax Ordinance: the whitewashing mechanism and parent pillar how Pakistan's FCY system costs the productive class $25 to 36 billion a year.

What the provision does

Inward foreign remittances received through banking channels are not subject to source-of-funds inquiry by the FBR

Remittances are not added to the recipient's taxable income for purposes of tax computation

The recipient is not required to explain the origin of the remittance

The provision overrides the general source-of-funds inquiry powers granted to the FBR under other sections

How the round-trip works

The 111(4) Round-trip

Step 1 | Domestic black money in PKR |

|---|---|

Step 2 | Convert to USD via trade mis-invoicing or hawala |

Step 3 | Funds arrive in Dubai/London/Singapore |

Step 4 | Park in foreign assets |

Step 5 | Send portion back as "remittance" |

Step 6 | Section 111(4) tax immunity applies |

Step 7 | PERA Section 5 prohibits source inquiry |

Step 8 | Money is now legally documented, tax-immune |

Frequently asked questions

What is Section 111(4) of the Income Tax Ordinance? A provision that grants tax immunity to inward foreign remittances received through banking channels, regardless of source. It prevents the FBR from inquiring into the source of remittances and from adding them to taxable income.

How much money is laundered through Section 111(4) annually? A 2018 tax compliance analysis estimated approximately $3.8 billion annually, based on the analysis that one-fifth of $19 billion in annual remittances is domestically generated black money being whitewashed.

Why hasn't Section 111(4) been repealed? Because it benefits the political and economic elite who use the round-trip mechanism to legalise offshore wealth. The same political class that drafts and passes tax legislation has historically had personal interest in preserving the provision.

Did the 2020 SRO close Section 111(4)? No. The 2020 SRO partially closed the rupee-to-dollar conversion pipeline at the deposit point but left Section 111(4) tax immunity intact and PERA Section 5 source-inquiry prohibition intact.

How does the Productive Capital Account address Section 111(4)? The PCA framework requires source verification on every deposit, exceeding both AMLA requirements and current PERA practice. PERA Section 5 would be repealed for PCA purposes. Section 111(4) would be revised to require source documentation rather than blanket immunity.

Sources

Income Tax Ordinance 2001, Section 111(4)

2018 tax compliance analysis on Section 111(4) whitewashing

2018 academic legal analysis of the AMLA-PERA contradiction

Yaseen Anwar, Governor SBP, statement on illegal remittances (October 2013)