The full breakdown, PKR 350 to 360 per USD for filers, PKR 365 to 385 for non-filers

By Asad Baig · Lahore · May 2026 · Approx. 5-min read

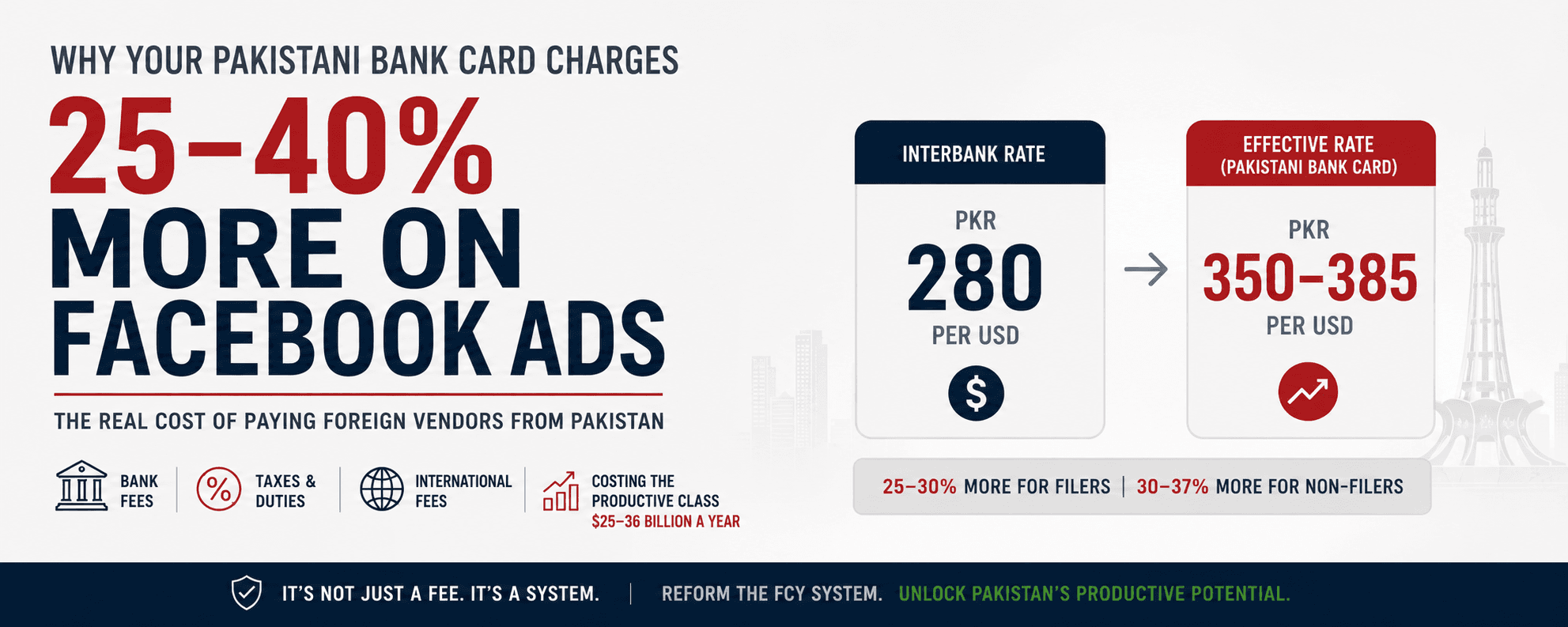

The short answer

For a tax filer at an interbank rate of PKR 280 per USD, the effective rate is approximately PKR 350 to 360 per USD when paying via Pakistani bank card, a 25 to 30 percent premium. For a non-filer, the effective rate is approximately PKR 365 to 385 per USD, a 30 to 37 percent premium. The premium is composed of bank conversion fee (3 to 5 percent), Federal Excise Duty (3 to 5 percent), Sales Tax on Services (13 to 16 percent), advance tax (1 percent for filers, 5 percent for non-filers), and international processing fee (1 to 3 percent), all stacked on top of the interbank rate.

This is a Tier 3 long-tail spoke under why your Pakistani bank card charges 25 to 40 percent on Facebook ads and parent pillar how Pakistan's FCY system costs the productive class $25 to 36 billion a year.

The calculation

$100 International Card Transaction, Full Breakdown

Interbank rate | PKR 280/USD |

|---|---|

Base PKR for $100 | PKR 28,000 |

Bank conversion fee (4%) | + PKR 1,120 |

Federal Excise Duty (4%) | + PKR 1,120 |

Sales Tax on Services (15%) | + PKR 4,200 |

Advance Tax, filer (1%) | + PKR 280 |

International processing (2%) | + PKR 560 |

TOTAL FOR FILER | ~PKR 35,280 |

Effective rate | ~PKR 353/USD |

Premium over interbank For non-filer (Advance Tax 5% instead of 1%) | ~26% |

TOTAL FOR NON-FILER | ~PKR 36,400 |

Effective rate | ~PKR 364/USD |

Premium over interbank | ~30% |

The numbers vary slightly based on the specific bank's conversion fee (3 to 5 percent range), the specific FED rate for the transaction type, and the specific provincial SST rate. The headline range of 25 to 30 percent for filers and 30 to 37 percent for non-filers covers the typical scenarios.

Where each portion of the premium ends up

Bank conversion fee, wire fees, card markup → Pakistani banks (~$1.5-2.5B/year)

FED, SST, advance tax → Federal Government (~$500-800M/year)

International processing fee → International card networks (Visa, Mastercard)

The vast majority of the premium is domestic. International card network fees are the smallest component. Pakistani-specific charges are what produce the headline 25 to 40 percent markup.

What this means annually for a productive earner

For a Pakistani entrepreneur spending $5,000 per month on foreign operational expenses (Facebook ads, AWS, software subscriptions):

Annual spend at interbank: PKR 16.8 million ($60,000)

Annual spend at filer effective rate: PKR 21.2 million

Annual extra cost: ~PKR 4.4 million (~$16,000)

This is the cost of being a Pakistani business that pays foreign vendors through Pakistani banking. Most companies of any size eventually solve this by maintaining offshore structures.

Frequently asked questions

What is the effective PKR/USD rate when paying with a Pakistani bank card? Approximately PKR 350 to 360 per USD for tax filers (25 to 30 percent premium over interbank) and PKR 365 to 385 per USD for non-filers (30 to 37 percent premium). The premium includes bank conversion, FED, SST, advance tax, and international processing fees.

Why is the rate higher for non-filers? Because the advance tax on international card transactions is 1 percent for ATL filers and 5 percent for non-filers. The 4 percentage point difference is meant to incentivise tax filing but in practice pushes non-filers out of Pakistani banking entirely.

What is the largest single component of the premium? Sales Tax on Services (SST) at 13 to 16 percent depending on province (Sindh and Punjab have different rates). It is the single largest line item in the markup.

Where does the premium money go? Approximately $1.5 to 2.5 billion annually flows to Pakistani banks. Approximately $500 to 800 million flows to the federal government in FED, SST, advance tax, and withholding taxes. A smaller share flows to international card networks (Visa, Mastercard) as standard interchange.

How much does this cost annually for an IT entrepreneur spending $5K/month abroad? Approximately PKR 4.4 million (about $16,000) per year in extra cost above the interbank rate. For an entrepreneur spending $20,000 per month, the annual extra cost rises to approximately PKR 17.6 million.

Would the Productive Capital Account eliminate this premium? Yes. The PCA framework exempts PCA transactions from FED, SST, and advance tax. PCA holders use international debit cards at normal global rates with no Pakistani markup, reducing the effective rate from PKR 350 to 360 per USD back to roughly the interbank rate plus standard international processing fees.

Sources

State Bank of Pakistan, regulations on foreign exchange transactions

Federal Board of Revenue, indirect tax collection breakdowns

Pakistani banks' international transaction fee schedules

Position Paper: The Foreign Currency Account Problem in Pakistan, May 2026