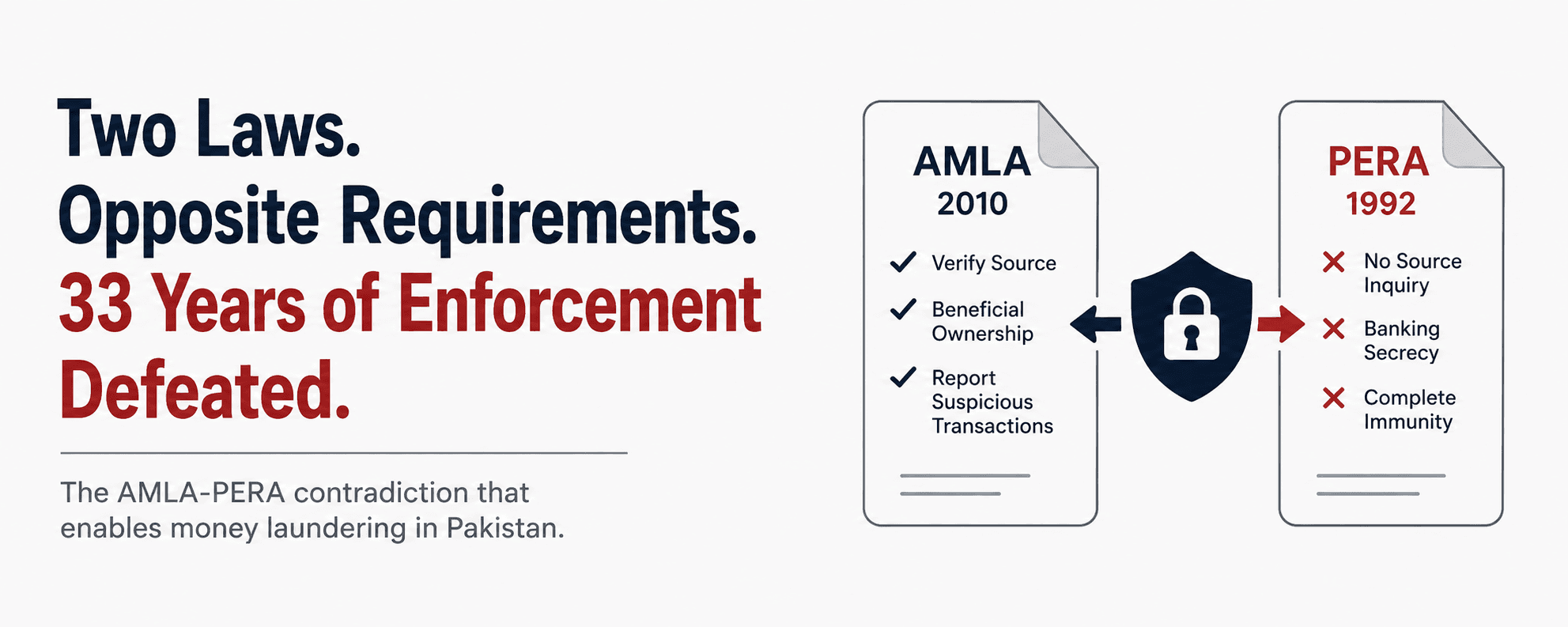

Two laws operating simultaneously with opposite requirements, defeating anti-money-laundering enforcement for 33 years

By Asad Baig · Lahore · May 2026 · Approx. 4-min read

The short answer

Pakistan maintains the Anti-Money Laundering Act 2010 alongside the Protection of Economic Reforms Act 1992. The AMLA requires source verification, beneficial ownership disclosure, and suspicious transaction reporting. The PERA Section 5 explicitly prohibits inquiry into the source of foreign currency deposits. Section 111(4) of the Income Tax Ordinance makes inward remittances tax-immune regardless of source. A 2018 Pakistani academic legal analysis concluded that "the objective of the AMLA to prevent money laundering is clearly defeated with the existing provisions of the PERA contained in sections 4, 5, and 9 of the PERA." This is published legal analysis, not interpretation. The contradiction has operated for 33 years.

This is a Tier 3 long-tail spoke under the AML-PERA contradiction: why I call it hypocrisy.

Frequently asked questions

What is the AML-PERA contradiction? The AMLA 2010 requires source verification. PERA 1992 Section 5 prohibits it. Both laws operate simultaneously in Pakistani legal system. The 2018 academic legal analysis concluded the contradiction structurally defeats anti-money-laundering enforcement.

What does PERA Section 5 do? Grants complete immunity from source-of-funds inquiry on foreign currency deposits, plus tax immunity and banking secrecy. Created in 1992, still operational.

What does Section 111(4) of the Income Tax Ordinance do? Grants tax immunity to inward foreign remittances regardless of source, preventing the FBR from inquiring into remittance origins.

How much does this contradiction cost Pakistan? Estimated $3.8 billion annually whitewashed through Section 111(4) alone, per 2018 tax compliance analysis. SBP Governor Yaseen Anwar's October 2013 statement put the broader figure at "over $9 billion" illegally remitted annually.

Did FATF compliance during 2018-2022 fix the contradiction? No. The reforms that hurt small users (KYC documentation) were implemented thoroughly. The reforms that would have exposed elite wealth (offshore disclosure, source-inquiry powers, beneficial ownership transparency that crossed jurisdictional lines) were implemented superficially. PERA Section 5 and Section 111(4) survived FATF scrutiny intact.

How does the Productive Capital Account address this? The PCA framework requires source verification on every deposit, exceeding both AMLA requirements and current PERA practice. PERA Section 5 is repealed for PCA purposes. Section 111(4) is revised to require source documentation.

Sources

Anti-Money Laundering Act 2010

Protection of Economic Reforms Act 1992, Sections 4, 5, and 9

Income Tax Ordinance, Section 111(4)

2018 academic legal analysis of the AMLA-PERA contradiction (Pakistani journals)

2018 tax compliance analysis on Section 111(4) whitewashing

Yaseen Anwar, Governor SBP, statement on illegal remittances (October 2013)